The Schwab Effect? | Revolutionising an Age Old Finance Product

The Schwab Effect? | Revolutionising an Age Old Finance Product

The case for Stablecoin saving products...

Hi All,

As you know by now, I love thinking about the future of finance.

Today is one of those days. But rather than reviewing neobanks (N26) or crypto companies (FTX, Argent or Kraken) I am looking at a 50-year-old ‘fintech’, Charles Schwab (‘Schwab’). Indeed, it was a “fintech” company before the word was coined.

In this post, I discuss Schwab’s fascinating business model before suggesting ideas on how newer fintech, and indeed crypto exchanges, can introduce a whole new product line - stablecoin interest rates products

Don’t worry, no talk about payout ratio, dividend yield or earnings per share here!

Never advice.

Deposits, deposits, deposits.

Following COVID-19, more people than ever before are investing. If not investing, more and more people are depositing their money with neobanks.

N26 Deposits | 46% CAGR FY19-FY21

In the past, I’ve written about how neobanks readily raise deposits and have suggested which product lines could be developed next (see here for my ideas!). But Schwab takes an entirely different approach.

Platform vs. Bank

A crucial revenue stream for Schwab is net interest income. I can hear your gasps, yes in the past 3 years (FY21, FY20, FY19), Schwab generated 43%, 52% and 61% of its revenues from net interest income. NB: the sharp decrease in FY21 is due to the acquisition of TD Ameritrade and its order flow revenues (page 63 of AR)

This is little surprise considering they have $7.3+ trillion assets under management and a market cap of $150bn+. Schwab does a lot… wealth management, securities brokerage, banking, asset management custody, and financial advisory services.

Despite seeming like an investment platform with a highly rated app (4.8 stars), still, net income is one of the most interesting parts of their business. Bear with me here.

The online brokerage market has been absolutely decimated. From fintech such as Robinhood to Schwab itself, buying equities is a land of no commissions. Instead, Schwab leans into earning interest on customer cash deposits.

Due to this, rather than being a platform/online broker, Schwab operates more like a bank - it has the full works, CET1 ratio (c.21%), capital requirements and indeed interest income.

Acquisiton of TD Ameritrade…

Following Schwab’s announcement that it’s getting rid of commissions on trading securities (Oct-19), its share price dropped c.9.5%. This was because back then, c.7% of its revenues came from commissions.

Well following this news, its competitor, TD Ameritrade’s share prices also fell -investors presume everyone would cut their commissions to keep market share. But it fell by 25% as c.36% of its revenues came from commissions.

While Schwab’s share price quickly recovered, TD’s didn’t and would you have it Schwab swooped in to buy TD!

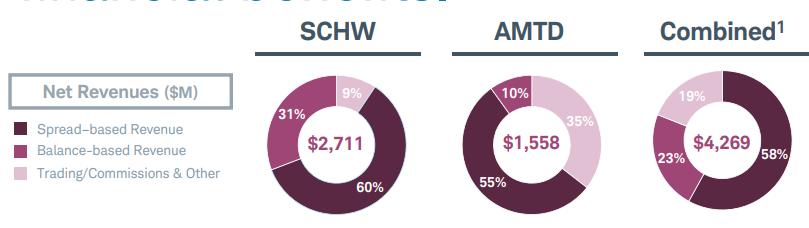

Perfectly executed (page 12), of spread based revenues (interest income) are drastically up…

While making up to $2.0bn in expense savings (page 14)!

What’s the Lesson Here?

Well, if you want to attract customers from incumbents, it is a no-brainer to charge zero commissions, right? People notice commissions! What do they care less about? interest rates. For many, it’s more rational to choose a broker based on low commissions rather than the rate they receive on their dollars.

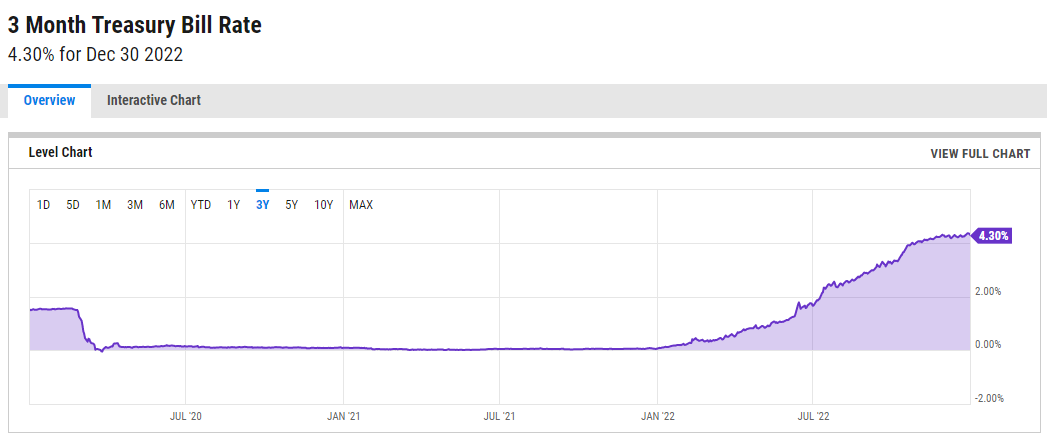

With the low-interest rate environment subsiding - US Treasury bonds are now c.4.3% - net interest income is *the* way to offset commissions.

First Derivative Impact | New Crypto Savings Product

Crypto exchanges should take this same approach but using stablecoins!

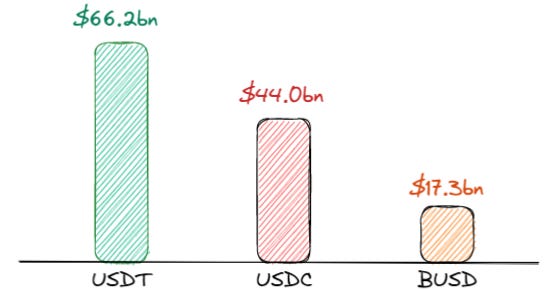

Below we can see the total value of relevant dollar-denominated stablecoins is $127bn. Source - Defilama

Let’s run a thought experiment. Using Nansen we see that crypto exchanges such as Binance ($27.7bn), OKX (c.$3.3bn), Bybit (c.$1.3bn), Crypto.com (c.$900m), Huobi (c.$600m) have significant amounts of stablecoins in their known wallets.

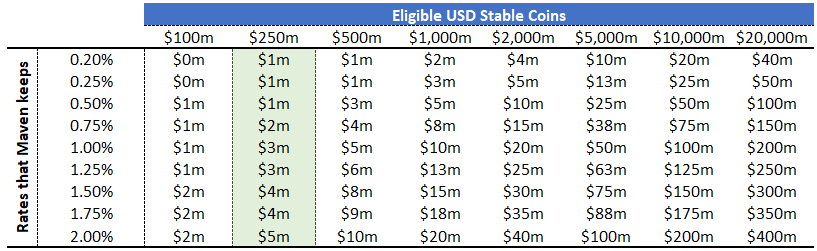

Let’s pretend we have a crypto exchange, “Maven”. It has $1bn of customers’ stablecoins (c.0.8% of all stablecoins). Let’s assume Maven’s users choose to send 25% of stablecoin assets to a new stablecoin savings product - $250m

Let’s assume Maven offers customers a saving product that yields 2%. By working with a bank or getting a banking license, Maven would be able to transfer $250m to the bank and hold it in US treasuries that yield 4.3%!

Let’s also assume that the technology and bank partnership costs Maven 0.7% of a $.

Therefore, Maven’s “Take Rate” is 1.6% = US 3M Yield (4.3%) - Customer Offer Rate (2%) - Tech and bank partner rate (0.7%)

Below we can see what the revenues would be on Maven collecting a range of 0.2% - 2% vs USD eligible amount for saving products.

As the number of eligible stablecoins increases with the growth in crypto GDP, this becomes very lucrative. It goes without saying that securing a partner bank and building infrastructure here is not easy.

As rates fall, Maven would offer lower rates until US rates are less than the partnership/infrastructure costs.

Schwab’ing Crypto Exchange Fees

You can guess what’s next. Let’s imagine Binance, elects to offer this savings product. At a 1.6% take with 25% of stablecoins being deployed to the savings product, they make $100m+

While this is not quite enough for Binance to completely send trading fees to zero, they can reduce their fees by a few %. This is great for users - particularly users that trade SIZE.

In other words, while such a savings product would not “Schwab” fees, it would reduce the fees while increasing stablecoin assets. This increases the trading volume that takes place on Binance for the cost of, increasing revenue?! Note that Binance likely has significant amounts of fiat also on their platform!

This is not a strategy that all platforms can use. As the crypto space grows and the total stablecoins in issue increase or indeed the US government issues digital dollars, you can bet your bottom dollar that this will be a product.

N.B. it’s worth noting that Coinbase has a stake in Circle, the creator of USDC. At current interest rates, they are set to collect $400m+ in revenues a year!

They also have a mountain of Coinbase cash ($5bn), a mountain of customer cash ($6.6bn) and a significant amount of customer stablecoins (estimate $9.5bn assuming stable coins are 10% of customer crypto assets). If these are put to work as underlined above, it’s a cash cow.

Saving Products vs Current Accounts

The difference between a Schwab account and a Chase current account is that while people tend to take money out of their current account, they are unlikely to take their money out of their savings/trading accounts.

Doubling this with the macro environment and cooling of trading, more people will hold stablecoins. The aforementioned crypto savings product would be the reason lazy users leave their capital on the exchange. Hereby, the exchange increases net interest revenue while increasing platform stickiness!

But it isn’t all roses (CET1)

One cannot simply become a black hole for stablecoins! As cash deposits accumulate, regulators would require the company to keep additional capital on its balance sheet to “back” significant amounts of cash from depositors. This is to protect from bank runs etc.

As there is no regulation or “CET1 Capital” in crypto, this product becomes murkier.

But we can use Schwab as an example.

While they have built a network of clients, offerings, and systems customer deposits have increased. It now has to make sure it has the regulatory capital and approvals to hold so many deposits. The complexity here can skyrocket but I’ll try to keep it simple.

Basically, as Schwab holds significant amounts of customers’ deposits, they have to have a certain amount of stockholders’ equity on the balance sheet. Stockholders’ equity is essentially the cumulative income that Schwab has accumulated over time.

In other words, this is effectively cash that Schwab owns and is not owned by customers. Rather than paying this out to shareholders, they have to accumulate this on the balance sheet. Latest results. Latest regulatory filing.

Schwab is unique in the sense that they keep wayyy more capital than is needed due to regulation:

Such a crypto product would require the same thing in order to get a bank license let alone even offer the product!

Forgetting commissions and rates, there’s another, more controversial, revenue generation avenue - payment for order flow. But we won’t get into that!

Conclusion

To close, with increasing rates, it pays to be asset-heavy. Coupling this with low payback to users, neobanks and indeed crypto exchanges can capitalise via offering saving products that increase the stickiness of their app. But in the largest crypto exchange’s case, by introducing my idea it can generate significant revenue from 2 avenues, trading volume (lower rates than competitors hence a larger market share) and interest income.

As usual, this is never advice but if you want to continue the conversation, message me on Twitter!

Thank you for reading!

Joseph - Jan 2022

NB: In Jun-22, Schwab’s Robo-adviser, Schwab Intelligent Portfolios, was fined $187m for over-allocating the amount of cash in the Robo-adviser portfolios (2015-2018). In fact, “the amount of cash that each SIP model portfolio contained was pre-set so that (Schwab) would earn at least a minimum amount of revenue.” Clearly, even Schwab had too much of a good thing.