N26 & The Future of Neobank Banking

N26 & The Future of Neobank Banking

Thoughts on the deposits problem, embedded finance, neobank valuations and more...

Hi All,

Despite the current market meltdown - in both public and private markets - one group remains smiling on a hill. Fintechs that raised series D+ in 2021.

Now that private market capital raises of $200m+ have dried up, these unicorns are not only well capitalised, but are also well positioned to (i) buy, (ii) build or (iii) invest/partner to extend their success further.

This blog post considers how N26, a German neobank that raised $900m @ a valuation of $9bn (Series E), can not only weather the economic storm but thrive.

Firstly, I summarise N26 then focus on “the deposits problem”, suggest solutions (payments and embedded finance etc.), before closing with commentary on a possible N26 exit + a summary of neobank valuations.

If you like my work, please reach out - @711_Joseph 👋🏾

Who are N26

Founded in 2013, N26 are an online-only neobank with 8m users in 24 markets. It has c.1,400 employees based in 10 locations across Europe, New York and São Paulo.

It has a German banking license and operates in 24 European countries including France (its largest market with 2m users), Germany, Italy, Portugal, Spain, Sweden and Switzerland. Despite this, it has recently closed its UK and U.S. businesses. Out of its 8m users, only 3.7m generate revenue.

N26 has raised c.$1.7bn to date from investors including Third Point Ventures, Coatue, Dragoneer, and Insight Venture Partners.

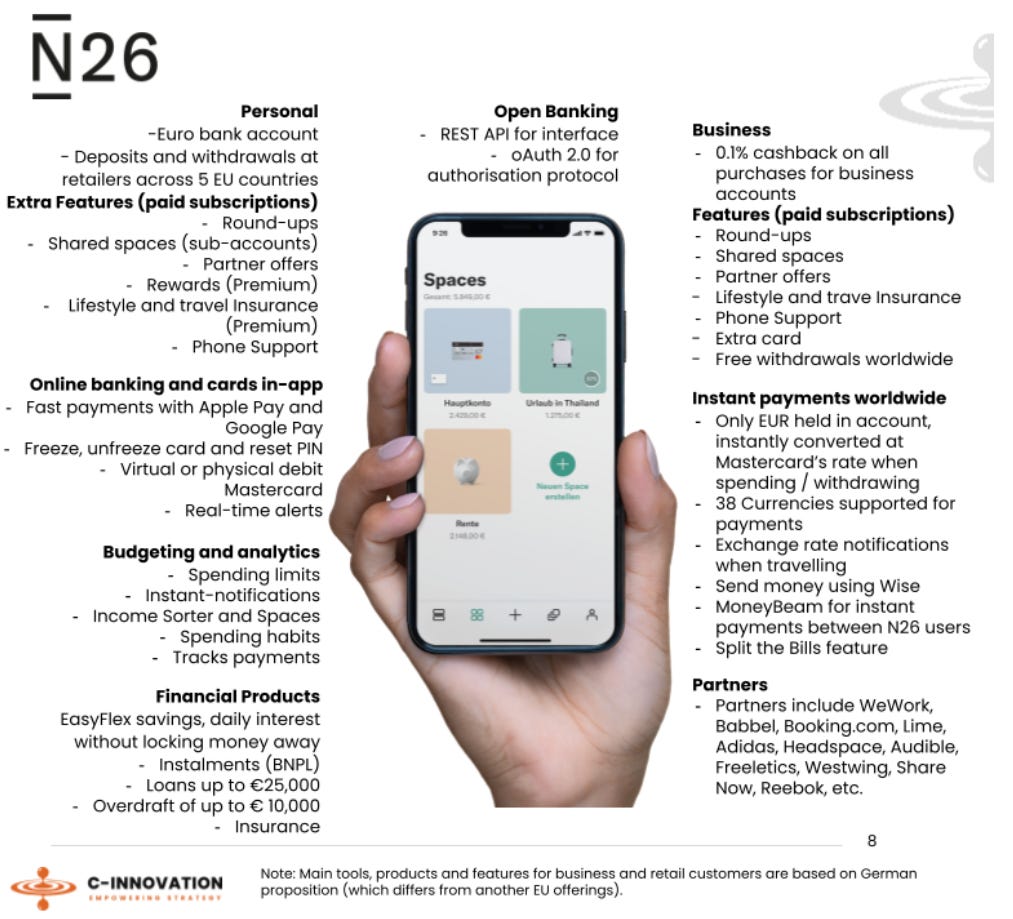

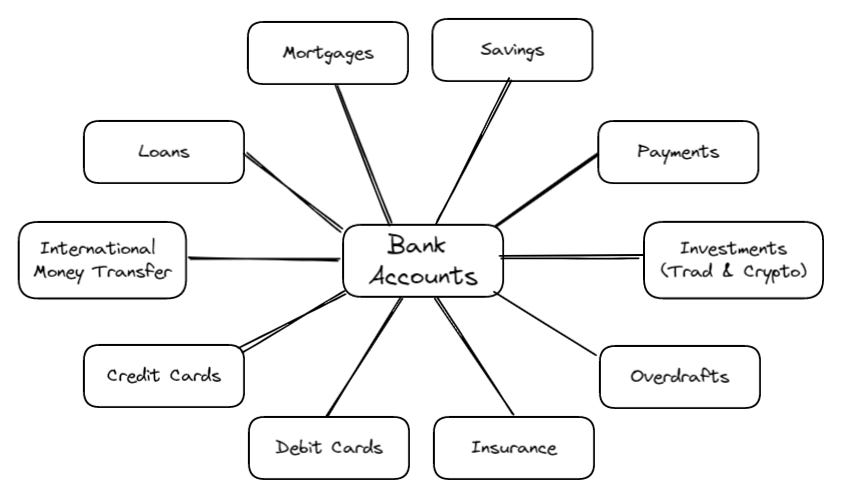

Products

N26 has a vast selection of products that you’d expect from your Neobank...

… and has historically partnered with other fintech companies to add new services. These partnerships are typically done via revenue share agreements.

N26 Business Model

N26 generates revenues via (i) card subscriptions, (ii) interchange fees, (iii) net interest revenue from deposits/overdraft products and (iv) partnership commission

N26 makes the majority of its revenue from its subscription-based card offering. Its services offering compounds/stacks respectively as the card tiers increase. Higher tiers unlock lower fees and travel insurance for instance.

Personal:

Business:

N26 also generates revenues via interchange fees. These are charges to merchants and other banks whenever N26 users use their cards for purchases.

N26 earns interest income from its deposits held by customers (these are generally interest rates passed back to users). It also collects interest income from its overdraft (€10,000 maximum, 8.9% p.a.) and loan facilities.

Finally, N26 generates revenue via partnership commissions. This is where N26 introduces its users to partners such as Lime or Booking.com. Its insurance offering falls here too.

Financials

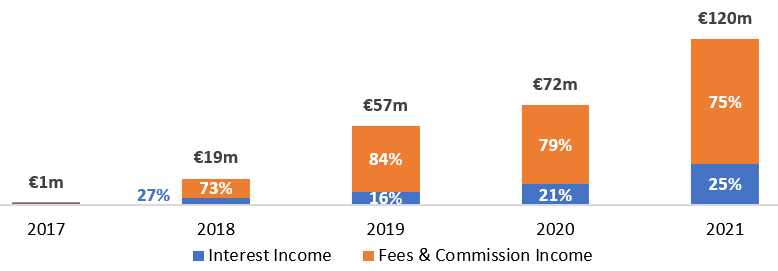

Its financials reflect those of a classic *successful* startup. Strong revenue growth (46% CAGR FY19-FY21) with increasing costs year on year. In 2020, c.45% (!) of its fees and commission income came from its card subscription products.

N26 struggles with profitability and remains loss-making - it lost c.€22 per customer in FY21.

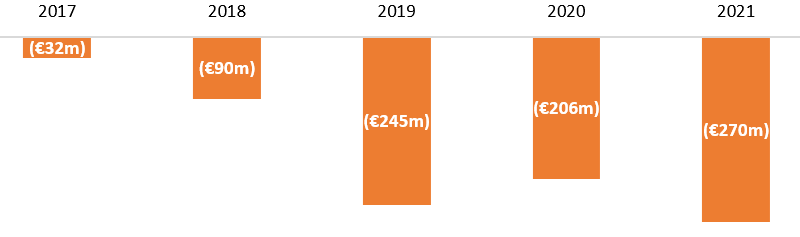

Despite this, its deposits growth has been outstanding and boasts €6.1bn deposits in FY21 (2020: €4.0bn) with 68% CAGR FY19-FY21. On average, customers hold c.€760 each in their accounts.

Revenues | 46% CAGR FY19-FY21

Admin Costs

Net Income

Deposits | 46% CAGR FY19-FY21

The Deposits Problem

This a double edge sword:

Neobanks are building sizeable deposits without a similar-sized loan book

And opposingly growth in deposits and loans would make these firms balance sheet businesses. Such businesses trade on a P/TBV (usually 0.4x - 1.2x) rather than EV/Revenue

Quite the quandary.

Challenge 1

Firstly, despite having €6.1bn in deposits, c.75% of N26’s revenues come from fee income! For traditional banks. Net interest income stems from interest on loans to users and interest rates from users' deposits.

On the one hand, as interest rates rise, N26 benefits if there are <100% interest rates income passback to consumers. On the other hand, neobanks, N26 included, have struggled to accumulate their loan books. This is due to a plethora of reasons - credit risk, regulatory hurdles and technological limitations being key reasons.

Despite this, more should be done to grow their loan books.

Challenge 2

With a burgeoning balance sheet, N26 must continue to be a “fintech at heart”. It should look to other verticals. While it is easy to “re-bundle” the bank stack, there are other avenues - most pertinent of these being embedded finance - that the bank can build/buy/partner with to control investor framing on focus their gaze on EV/Revenue (as well as EBITDA margin!)

Fundamentally, N26 is well funded (€900m capital injection + €6.1bn in deposits) but has nothing to do with it.

What's Next for N26?

At this point, N26 has saturated the typical neobank offering. But other opportunities are out there.

In the order of perceived difficulty, N26’s options are:

Lean into partnerships and target a “super-app” offering

Reduce partnerships by bringing more services in house

Acquire a brokerage or price comparison platform

Build an embedded finance offering

Crypto

Option 1: Super App!

Without labouring the point, super apps are… an app of apps. See below for Revolut’s offering. While they’re a bank/payment card, they also offer many other services. The idea is with these, they become a daily app with high touch points and eventually a significant amount of valuable customer data (cross-sell anyone?).

Below is Revolut’s offering - it’s worth noting that they were valued at $30bn+ before they added many of these.

As Revolut has done, N26 can create a super app. It can continue its large number of partnerships and add further options. N26 is well-positioned to bundle it all.

Crucially, N26 should take time to consider its tech stack build-out - insuring there is the scope for an internal build out/a “universal connector plug” that is compatible with other providers as partnerships come to an end.

Option 2: Partnerships No More?

While partnerships enable N26 to have a high speed to market and limit costs, what happens when if counterparties are acquired or worse, they decide to stop the arrangement with N26?

As companies (startups) become starved for capital, an M&A roll-up strategy focused on the above diagram brings talent and expertise in-house.

To begin, N26 can focus on:

Savings products:

Risk: High interest rates on deposits is lucrative. However, without sufficient passback of these rates to customers, customers may take a mercenary approach and simply bank with other banks with better terms

Lending:

Risk: Credit risk. N26 must first decide on its target customers. In a recession, sub-prime customers may increase impairments, hurting medium-term profitability metrics. High-interest rates may negate this impact however

Insurance

Risk: Many insurtech startups are collpasing. N26 must consider both customer-side relationships as well as relationships with insurance providers. N26 should also refrain from carrying insurance risk on its balance sheet. Any M&A should be of brokers only. It should also watch out for “burning $1 to make 90¢”.

Investing/wealth

Risk: In the current macro backdrop, would consumers still be using such products? The payback period may be extended. Ongoing fee compression is another consideration, especially as revenues only materialise with sufficient scale. Startup leaders in the space have a relatively low AUM/customer compared to peers (see Robinhood vs Charles Schwab)

Crypto

Risk: N26 must consider ongoing dialogue regarding what constitutes as a token/“security” and further regulation. N26 should watch out for companies caught in the Celsius/Luna collapses and any repercussions from buying such companies - legal and otherwise

Option 3: Brokerage or Price Comparison Platform

N26 could acquire (reverse merge?) a mortgages broker or a price comparison website

Mortgage Brokers

Rationale:

Problem:

N26 needs to build out its loan book

Mortgages are often a large part of a bank’s loan book

However, customers are unlikely to choose a neobank for their mortgage

Solution:

Thankfully, arranging mortgages is a broker’s business. While banks do provide mortgages directly, the first step to many agreements is via a broker

There are two types of broker business models - charging only the lenders commission on agreements closing, or charging both lenders and the customer an upfront fee (with auxiliary services in place)

For instance, L&C Mortgages & Trussle are free to use as they charge lenders a commission

But Trinity Financial, Fluent Money and Mortgage Advice Bureau may charge a fee on both sides

With time, N26 could acquire regional mortgage providers and launch as an online-only provider of mortgages on its broker’s platform - however, there may be stringent regulatory hurdles

It could also use that as a platform to offer consumer loans

Other Benefits

Such an agreement would enable N26 to gather data on users and may increase app stickiness/usage due to its link to such an important purchase (a home) for the average person

They would also ensure repeat usage as they can reach out to homeowners when their fixed mortgage period is over (typically every 2 -5 years)

Brokers spend money on marketing. This would be massively reduced with N26 branding and its current userbase

Risks:

Mortgage volumes may drastically reduce with recently higher rates and more stringent credit profile requirements

Getting mortgages providers on the platform could prove tough

Do N26’s users want to use them to search for a mortgage? Is this what the profile of its current users wants?

What happens to users with a worse credit profile than what N26 services?

Price Comparison Platform

This is simpler.

Rationale

Problem:

The world is seeing rampant inflation with the cost of living costs spiralling

Price comparison platforms attempt to out-compete each other and most of their costs are marketing related

Solution:

N26 builds/buys a price comparison engine focused on “day-to-day” items/bills (energy, heating, gas) and usual things such as internet broadband, insurance etc.

N26 has a visual of what its users spend money on. Should a user agree, N26 would show them places and ways that they can save money or buy “higher quality” items from alternative means

N26 can “ping” users whenever they can save on repeat purchases

It then receives a commission for its new customer’s funnels

It also would not spend as much on marketing as its competitors do because it already has customers and such a service could spread via word of mouth

Other benefits:

More touch points for users and increases the usage of its app

Could also offer tiers as add-ons to its subscription cards

Cards become a “no-brainer” if such a subscription would save more money than it costs

N26 simply captures more and more user data and can build an engine that would offer better and better-targeted services/products to users. Ultimately can become “predictive” of behaviours

These are both in line with N26’s mission

N26 prides itself on offering deeply personalised banking experiences and both of the above increase this!

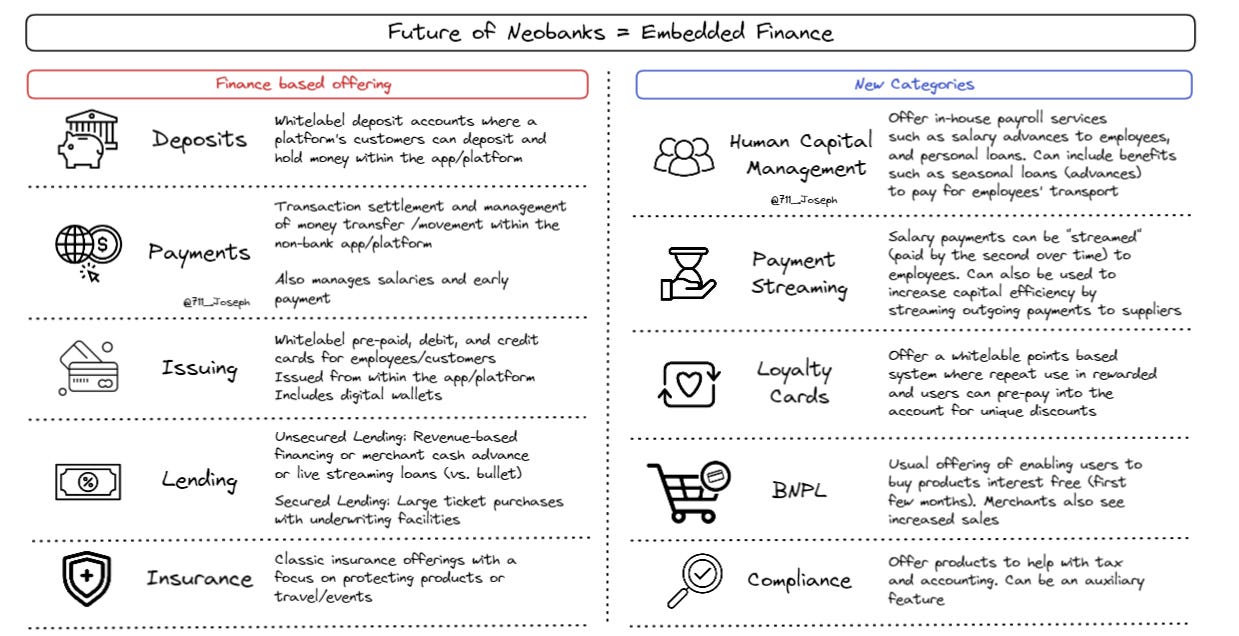

Option 4: Embedded Finance

Revenue growth can also come from increasing transaction volume via an N26 embedded finance platform offering.

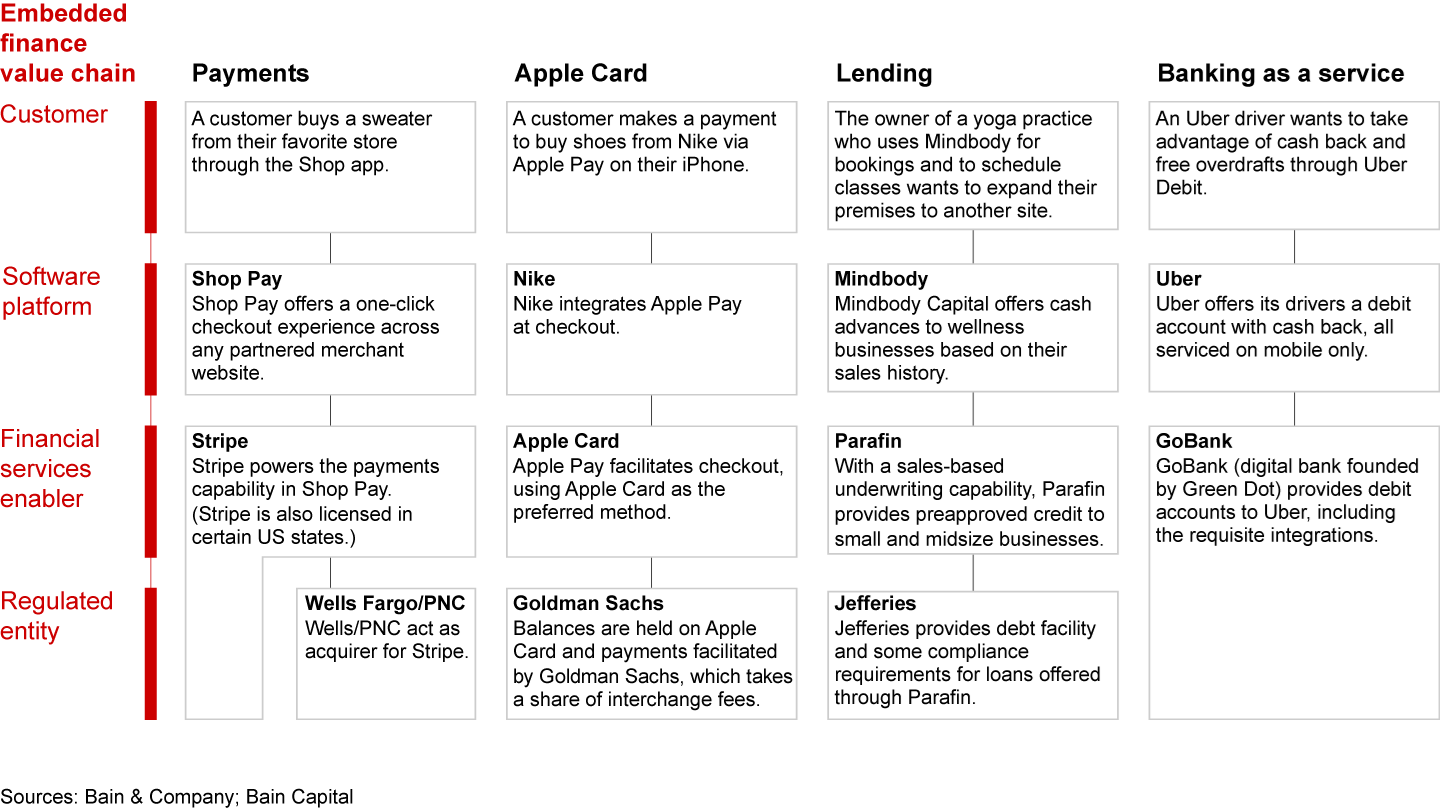

What Is Embedded Finance

Embedded finance is the umbrella term for financial products placed within a traditionally non-financial app. Traditional finance institutions typically do not play a part here.

For instance private-label credit cards at supermarkets/airlines or BNPL services in e-commerce or even Uber debit cards. More examples are below.

Why Even Bother With Embedded Finance?

It’s a classic case of enabling companies to focus on things that “make their beer taste better” rather than complex challenges that don’t.

The value proposition is:

Embedded finance services may help platforms to reduce their costs + costs for their users…

.. while also enabling platforms to leverage proprietary customer data to unlock new financing use cases which are highly relevant to its users.

Customers, therefore, benefit from contextual seamless experiences…

… while access to novel products may increase user’s options and personal liquidity

What Would A Neobank Embedded Finance Offering Look Like?

While any potential neobank embedded finance offering would have financial engineering/products at its core...

… there are many other categories prime for disruption:

Galileo is a slightly mature example of this neobank future. It offers secured credit cards, virtual cards, debit cards, EMV chip cards, prepaid cards, payroll cards, contactless cards, and rewards/incentive cards.

The “best of” embedded finance are products with trivial integration and minimal resource requirement.

Embedded Finance | End Game

Via an embedded finance offering, N26 could create a double-sided funnel to reach end customers.

All of these result in an app that can (a) generate contextual data, (ii) access and identity banking/transaction data (c) aggregate this with e-commerce data and (d) process adaptive analytics…

Resulting in a predictive app.

With the boom of the “unbundling banks” thesis among startups, today there are many companies that are likely running out of financial runway. Thus, they are “rebundling” targets for N26.

Option 5: Crypto

Is it really Joseph’s thoughts blog without a comment on crypto?!

*** As I was writing this blog, N26 announced a crypto offering via a partnership***

In short, away from simply buying and selling/investing in crypto customers will eventually be able to:

Buy day-to-day items using crypto (Revolut just announced this)

Leverage crypto for cheaper international money transfers via blockchain rails

Use defi products to lend (deposit for yield) or borrow as defi scales and matures

It is critical that any such services do not use Cefi products. See Celsius and how it effectively caused Nuri to shut down

In the current market, there will be several crypto companies that run out of money! N26 can be opportunistic to acquire the team & tech needed to build out the above functionality.

Risks Risks Risks

While these options sound good and (I am sure you now agree) have merit, they may distract from the core business and dilute the brand if not done well.

Similarly, it costs capital to launch new business lines. With capital no longer being ~free, capital would need to be freed from superfluous products or regions.

Still, if these are such good ideas, competitors are already working on them! Railsr. OpenPayd and Solarisbank have stellar embedded finance options. How can N26, or any neobank know that they are up to the task?

Perhaps focusing on extending their own “as is” runway without any of the above!

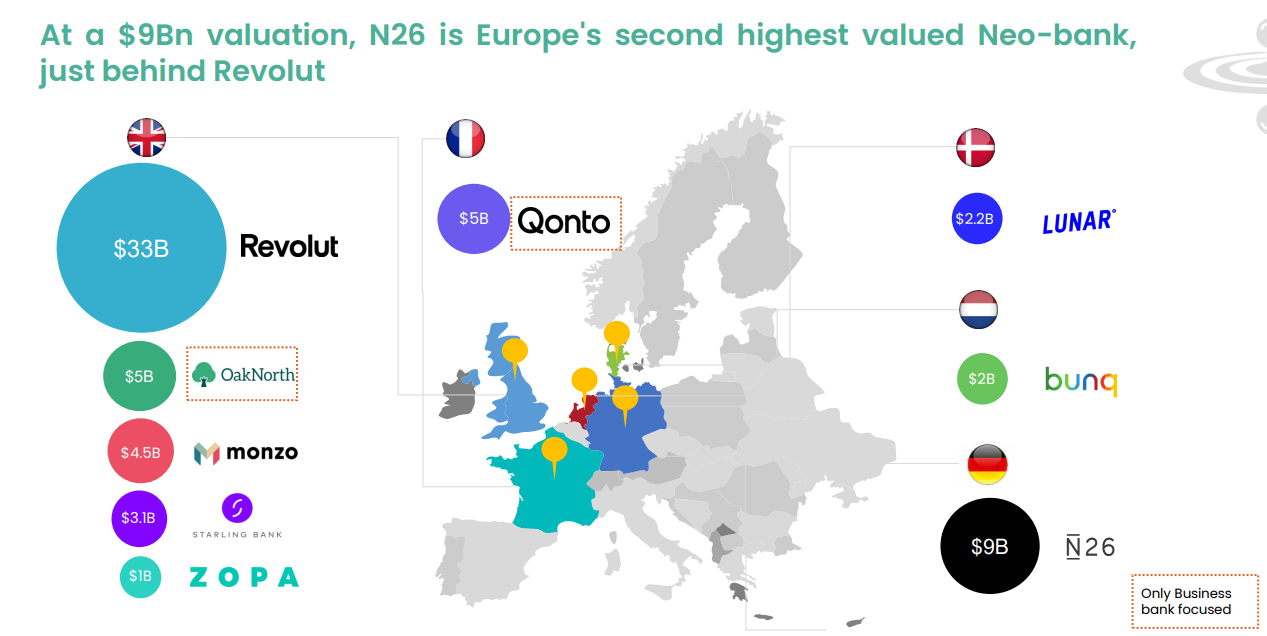

Valuation | What does exit look like?

To date, N26 has raised $1.7bn from investors including Third Point Ventures, Coatue, Dragoneer and Greyhound Capital. Its most recent capital injection was its series E where it raised $900m at a $9bn valuation.

This makes N26 the 2nd highest-valued neobank and one of the most valuable European tech companies.

IPO?

At this size, the only realistic next step is to IPO.

N26 was rumoured to have been planning for an IPO by 2022/23. Conventional wisdom and current market sentiment suggest that this will not be on the cards until at least 2024+. Thankfully, N26 is well capitalised to ride the storm until then.

Before closing, here’s the latest on Neobank valuations. Sources are available upon request.

Other Neobank Valuations

These are the bank’s last rounds. “x5 is the new x10”. All data is the latest available (i.e. some 2020). These were manually scrubbed and did not use Pitchbook :)

EU Neobanks

Atom Bank

Was considering a SPAC merger on the New York Stock Exchange at a valuation of $700 million

Feb-22: Raised £75m @ £435m valuation

Revenue: c.£11m | NII represents 95%+ of revenues | Loan book: £1.5bn+

Monzo

Jan-22: Raised $600m @ $6.5bn valuation

Revenue: c.£60m | F&C makes c.65% of revenues | Loan Book: < £100m

N26

Oct-21: Raised $900m @ $9bn valuation

Revenue: c.€120m | F&C make up 75% of revenues | Loan Book: Zero!

Revolut

Jul-21: Raised $800m @ $33bn valuation

Revenue: c.£220m | 70% of revenue come from card & interchange and subscriptions | Loan book: <£1m

Starling Bank

Apr-22: Raised £131m @ £2.5bn valuation

Jupiter sold its stake in Starling at a steep discount - rumoured to value the company at £1.5bn

Revenue: c.£70m | NII makes c.60$ of revenues | Loan book: £2.2bn

Starling built its loan book due to the UK government’s COVID-19 scheme. It is yet to be seen how they will keep these levels up + if they adequately screened the credit risk of its customers

Monese

Sep-22: Raised $35m @ an undisclosed valuation

Revenues: c.£16m | 100% of revenues come from F&C

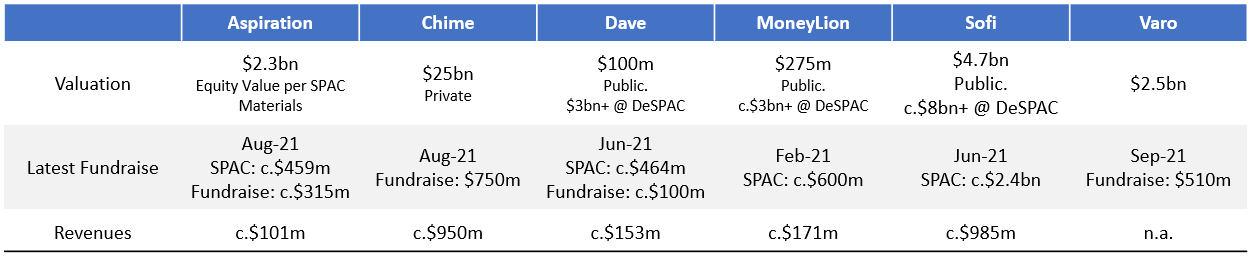

US Neobanks:

Other

Lendable - Raised £210m @ $3.5bn valuation (Mar-22)

Zopa - Raised £220m @ £750m valuation (Oct-21)

Captive Banks - Neobanks within larger banks

Boursorama - €1.1bn (2015 acquisition)

Comdirect - €1.8bn (2020 acquisition)

Marcus - $2.8bn (early 2022 brokers’ note (SOTP of GS))

LatAm

Nubank - c.$20bn (public) | IPO - $2.6bn raised @ $41.5bn valuation (Dec-21)

C6 Bank - $2.2bn (BRL $11.3bn) (Jun-21)

Neon Bank - $1.3bn | Raised $300m

Acquisitions

JPM bought nutmeg : £700m in Jun-21

Wealthfront had agreed to buy Welathfront for $1.4bn but this deal collapsed

Betterment - Raised $160m @ $1.3bn valuation

Conclusion

Clearly, we are far from the end game of neobanks. There is still much to do and opportunities to revolutionise the segment further. While there is no longer a rush to grow at any cost and profitability comes into focus, as shown, well-capitalised neobanks/payments-based fintech have a plethora of options to take their offering to the next level.

Thanks for reading.

JS - 7th November 2022