Kraken | Pre-IPO Investment Case

Kraken | Pre-IPO Investment Case

Could a bridge c.$300m warchest be the catalyst for a $10bn IPO...

If you like my work, please reach out - @711_Joseph

Hi All,

I believe crypto is the future.

In that future, people need crypto “wallets”. I focused on that in my first research/investment piece on Argent.

Before users get a crypto wallet, centralised exchanges (CEX) like Coinbase or Binance are *the* gateway to the world of crypto.

However, a third CEX player - Kraken - may be uniquely placed to capitalise on the leaders’ weaknesses and grow as the premier “all-things” crypto platform.

Here’s my second full-on research piece on Kraken. Considering a minority investment by growth equity player(s) ahead of a potential IPO

Not advice + represents my views only.

Summary

As the investment committee of Growth Equity Fund I considers its first crypto investment, we recommend against engagement with the Kraken team regarding the formation of a total $300m pre-IPO investment.

While Kraken has created a strong exchange for trading digital assets, fierce competition from Coinbase and Binance and underwhelming outside-looking-in metrics suggest that Kraken will be left behind.

Counter Consideration: However, while the crypto market is still nascent we are impressed by Kraken’s focus on regulation and speed to market. As blockchain technology comes to the fore, we see an opportunity for Kraken to establish itself as a platform with a focus on alternative additional offerings.

Ahead of any engagement, we would like to see (i) Kraken’s user metrics and retention over time, (ii) its plan/early actions on a path to profitability in the medium term and (iii) a plan to cut costs in a “crypto-winter.”

Overview

Kraken is a cryptocurrency exchange platform based in San Francisco, USA. It offers spot and futures crypto trading for users to buy, sell and trade crypto assets. It has 3200+ employees (Jun-22).

Kraken targets retail users, professional investors, and institutions alike. Through two apps, “Kraken” (retail/newer users) and “Kraken Pro”, users can trade 185+ digital assets ranging from Bitcoin to Curve and 8 fiat currencies (GBP, EUR, USD, CAD, JPY, CH, AED and AUD). Kraken is available in 190+ countries, including 40+ European countries. Europe is its most significant market.

Founded in 2011, Kraken boasts 9 million users (Jun-21: 6 million, Feb-19: 4 million) and recorded $601bn in transactions in 2021 and $195bn year to date. We estimate that Kraken holds $9.2bn of users’ assets as of Jul-22 but this is down materially from our Feb-22 estimation of c.$30bn.

Kraken prides itself as a regulation-compliant exchange and holds most user deposits in air-gapped, geo-distributed cold storage. It has never been hacked. Kraken is registered with key regulatory bodies such as FinCEN (US), FINTRAC (Canada), FCA (UK), and AUSTRAC (Australia).

Kraken is the fourth largest CEX, after Binance, Coinbase and FTX according to CoinMarketCap. Though Nomics suggests that Kraken is the 10th biggest CEX by YTD volume.

In the tech valuation boom of early 2021, Kraken was rumoured to target further funding/IPO @ a $10bn valuation but this did not materialise. For context, Coinbase’s market cap is c.$15bn (IPO’d @ $65bn)

1. Product

Kraken primarily offers cryptocurrency trading and subscription-based trading services. Auxiliary services include cryptocurrency staking, parachain auctions and OTC desk ($100k min order size) services.

Kraken offers a crypto exchange where users trade crypto. This takes the form of both spot, crypto indices, and derivatives (futures) with Kraken also offering margin trading. Margin trading is offered only to clients outside of the U.S. who are at the “intermediate and pro” verification levels (though this is only self-verification in the UK). It also offers an “Advanced Trading” / “Account Management” subscription service.

Kraken also offers up to x5 margin crypto trading (liquidates at 40% LTV). Only “5 - 10%” of users use leverage. It does not offer x100 gambling speculative products as some competitors do. Kraken has a waiting list for its planned NFT offering.

Staking

Some blockchains are validated via “proof of stake” (POS) rather than “proof of work”. In POS, to validate the transactions, users can “stake” their crypto in return for a payout. Kraken consolidates + stakes on its infrastructure on behalf of consenting users. According to Dune Analytics, Kraken manages 8.3% of the staked ETH (Lido @ 30%, Coinbase @ 14.5% and Binance @ 6.6%).

2. Business Model

We expect that most of Kraken’s revenues come from transactions (trading). There is no substantive colour on revenues from other services.

Leaving aside its aggressive instant buy fees, Kraken’s transaction fees range from 0% to 0.26% and depend on a user’s 30-day trading volume. Considering a blended fee of 0.24% (assumed) and Kraken’s trading volume was c.$600 billion in 2021 and c.$207 billion last quarter (as of Sep-22), this suggests that Kraken generated revenue of c.$1.44 billion in 2021 and c.$0.5bn in the last quarter.

Sensitivity revenues for blended fees:

Considering the macro backdrop, lower volatility and depressed prices, it is easy to predict these revenues may be lower in the shorter term. Similarly, there may be further fee compression as competition increases.

Staking Revenues:

As aforementioned, Kraken enables users to delegate their crypto assets to be staked on their platform. This removes the need for technical know-how and the need to have threshold amounts of a certain asset to stake. For this benefit, Kraken retains a portion of the yield earned from staking, though strangely they only take a fee for $ETH staking (15%). Coinbase’s staking fees range from 8% to 25%.

Kraken has a wider staking offering (17 tokens) compared to Coinbase (7 - ETH2, Tezos, Algorand, Cosmos, Cardano, Tether, and Solana – all are offered by Kraken).

Following the merge, Ether staking is an opportunity to grow revenues over the longer term. Kraken began staking $ETH in Dec-20 and to date stakes c.1m $ETH (8.3% market share) across 36.4k validators.

Assuming: (i) the yield on staking Ether is 5.2%, (ii) Kraken has deposited 1,142,368 $ETH (Dune Analytics), (iii) $ETH token price of $1,325.83 & (iv) a Kraken admin fee of 15%... projected revenue is only $11.8m.

Once the Ethereum merge allows reversible staking, thereby increasing liquidity, staking Ether may materially increase revenues. Naturally, Ether token prices drive this revenue stream. While Kraken’s decreasing market share for staking $ETH has stabilised, staked $ETH already consists of c.50% of the $ETH held by Kraken. Without a meaningful increase in $ETH prices & $ETH staked per user, there is little upside.

Other Revenue Streams:

These include the larger staking and predictably smaller avenues such as (i) custodial fee revenue, (ii) interest income from custodial fiat funds held at third-party banks and (iii) crypto asset trading revenue from Kraken’s OTC trading desk.

3. Team

Chairman & Co-Founder - Jesse Powell

Serial entrepreneur founded Kraken in Aug-11 | Stepped down from CEO role in Sep-22

View: Very able with enigmatic entrepreneurial zeal. Comes across as considered and steady in interviews but is very publicly outspoken (Twitter). Impressive mix of technical ability & selling acumen

CEO - Dave Ripley

Current COO of Kraken, hired after 1-year internal & external executive search (Sep-22) | Joined Oct-16

Joined Kraken via its acquisition of Glidera, a crypto wallet funding service where he was a co-founder and CEO. Started his career as a software engineer and product manager, before joining BCG. Successfully grew Kraken from 50 to 3,200+ employees, has completed 16+ acquisitions and secured regulatory licenses and partnerships

View: Well-equipped and experienced to lead Kraken into its next chapter. Probably the best person that they could have hired for company “know-how”. Though may Kraken need someone with a fresh perspective and is not saddled by a “status quo”?

Aims to “continue to invest in the ongoing expansion of [Kraken’s] product portfolio” and does not agree with large costly marketing projects that were run by competitors (Crypto.com $700m naming rights deal)

4. Risks

Public perception of Kraken’s brand and culture

Simply put, the ex-CEO of Kraken has been vocal on a range of topics. Some of which - Russia, USA, woke culture, etc. - may leave a sour taste for potential users’ or stigmatise the company

As part of this, the ex-CEO offered unhappy employees a “Jetski” (severance package) to leave. Though Jesse confirmed that only <40 / 3,200 employees accepted this

Current regulatory scrutiny and public perception of such news

Similarly, despite positive regulation acceptances and mandates, Kraken somewhat regularly is in the news for investigations - though the reliability of such allegations varies (perception is enough to hurt Kraken). Example: Kraken Under Investigation for Alleged Sanctions Violations: Report

Brand recognition

Globally, Kraken is a laggard and has not had similar breakouts as Coinbase and Binance

Token Selection

Initially, CEXs differentiated themselves by the types of coins that they offer but this is not as much the case anymore. However, with increased token/security scrutiny from the SEC, this may leave trading of exotic tokens with decentralised exchanges. That said, new competitors such as Robinhood barely have a crypto offering

Maintenance

Tradfi exchanges can complete maintenance during the evenings. However, the crypto markets are 365 days / 24 hours meaning maintenance is tough. Downtime or bugs may be material for users

Focus on professional investors and institutions

Kraken has historically focused on large professional traders/institutions heavy. Though these users have bigger cheque sizes, they are more price sensitive to fees and hence fees are typically lower

A shift to retail may be more worthwhile (as seen by valuation differences between PayPal and CME Group) for instance. Competitors such as Coinbase focus more on higher-fee retail investors

Criminal activity

Part of any centralised exchange’s secret sauce is its KYC process. It is close to impossible to meet 100% prevention but Kraken can add significant transparency and rapid process to probe bad players

Chainalysis has a relevant report touching on this further

5. Industry Observations

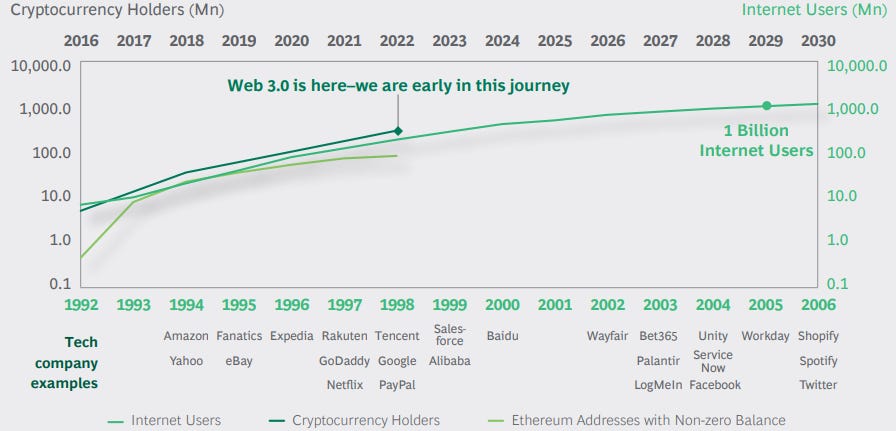

It’s still only the beginning…

Considering the global population, market penetration is low. There remains a significant opportunity for centralised exchanges - especially as they are typically the gateway to crypto. There are only c.90m+ users across major exchanges. This number comes down further considering a user may have multiple accounts.

Similarly, retail adoption has progressed at a rate faster than that of internet users. Recent reports suggest that crypto will reach only 1 billion users in 2030.

To put this into perspective, there are c.5 billion internet users globally and only 2.5m DAUs in Web3 across blockchains

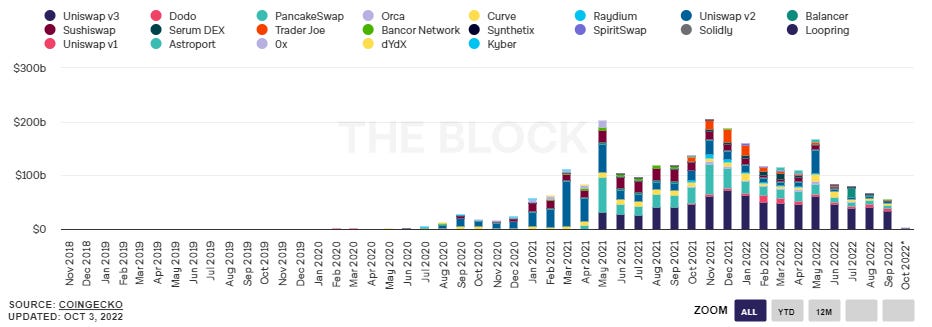

… and even though spot trading is down…

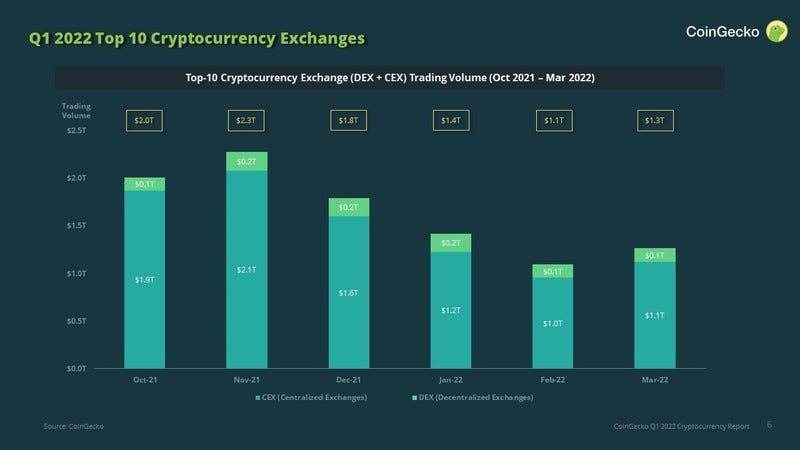

… CEX volume has stabilised at multiples higher than pre-2021 levels…

While centralised exchange volumes have cooled off, they have reached a new normal that is multiplies higher than 2020 activity.

CEX's global trading volume in 2021 was c.$14,000 billion. Note that some smaller exchanges may artificially inflate their numbers. Kraken had $601bn trading volume in 2021. This suggests a c.4% market share among centralised exchanges. Comparatively, in 2021 Coinbase announced FY21 in trading volume of c.$1,671bn (c.12% market share) and c.$6,837m trading revenue - we had calculated Kraken transaction revenue to be c.$1.44bn in 2021. Compared to Kraken, Coinbase has c.8% more market share and 2.8x more trading volume and 4.7x the trading revenue.

… Still, as the number of MAUs level out …

Despite the sharp downturn, x4 the number of users remains compared to the last bear market.

…there remains lower than expected CEX to DEX user conversion…

DEXs are an alternative to CEXs. Still, DEX users are well below that centralised exchanges. For instance, the most popular decentralised exchange, Uniswap (62.3% market share by volume) has only had 4.3m users ever (again be conscious of double counting) according to Dune Analytics. Point is, people do not usually “graduate” from CEX to wallets. The technological hurdle could be the reason for this.

… amidst relatively muted volatility and increasing correlation to trad-fi.

In Contrary Research’s note on Kraken, they share: “10 of the most popular cryptocurrencies command ~80% of the market. Movements in the top 10 cryptocurrencies significantly impact the value of trades in the market.” This suggests that while one-off surges in lesser-known tokens generate significant revenues, volatility across the largest coins is the driver for significant revenue. Similarly, according to CoinGecko, in Q2’22, the top 30 crypto market cap correlation with the S&P500 was 0.92 (high correlation) in Q2 2022. This was an increase from the correlation coefficient of 0.72 in Q1 2021. As the macro outlook sours, CEXs may see reduced revenues for the long term (due to lower asset prices) despite the impact of heightened volatility in such a market.

New Kraken Product | NFT Offering

As Kraken attempts to launch its own NFT offering, note that NFT volumes have fallen 97% from summer highs. Considering the users that are still active, only 40% of NFT buyers use Solana despite its lower gas fees and promise of faster and cheaper transactions. Even as all of the NFT value sits on the Ethereum blockchain.

Nonetheless, Coinbase released its NFT offering a few months ago and it is simply not used as seen below.

6. Strategic Suggestions / Ideas

Clearly, Kraken is not the biggest platform nor the most popular. However, it could still benefit should it continue to innovate its offerings (like it did with Polkadot’s parachain auctions). Only then can it continue to grow with the market. The following is shared humbly.

Launch or acquire a Crypto Wallet

While Metamask is in the lead with 30 million users, a wallet offering may increase the stickiness of the Kraken brand. Users can “graduate” from a CEX to a DEX yet stay in the Kraken ecosystem. Coinbase offers a crypto wallet already (Coinbase Wallet)

This approach may not generate value instantly but prepares Kraken’s pipeline to connect its users with defi, staking, and the next frontier of crypto products. An integrated Kraken Wallet may allow tech newbies to access dapps all within the Kraken ecosystem.

Strategy:

Partner with several of the smaller wallets and offer to (i) add Kraken’s transaction settlements to their trading aggregator or (ii) be a white-label swap settlement layer for them

Should the relationship go well, Kraken can invest in the company

Once product-market fit nears, acquire the wallet and rebrand it into a Kraken Wallet

I suggest an investment in Argent – Kraken can offer to be an extension of Argent’s series B.

Launch a dapp store focused on "emerging", or “next billion users” markets

Target markets such as India, Indonesia, Brazil, Nigeria, South America & the Caribbean.

Create a platform that enables engagement with new-age finance and currency conversion services within the Kraken ecosystem. Kraken may list external providers too and charge a commission

Any such solution must be based on layer 2s due to gas fees.

L2s (Arbitrum & Optimism) account for 30-40% of all transactions on Ethereum but consume only 2% of the total gas. Ideal for these regions.

Banking licence

Kraken can take advantage of its banking licence and offer a custodial banking service. Albeit launching as a small outfit, near-term higher interest means that this is a revenue-generating business from day one

Kraken is the only CEX to have obtained a Special Purpose Depository Institution (SPDI) charter (Sep-20). Kraken will be able to provide some banking services such as crypto debit cards, but cannot use customer deposits to issue loans as it is a “custody bank”.

In the future, Kraken may charge users fixed fees for services, such as wires and bank-to-bank transactions. In other words, this SPDI charter allows them to act as an on/off ramp to the banking ecosystem.

Strategy:

Once Kraken prove this is successful, either (i) push for a licence for loan capability/services or (ii) partner with larger banks/institutions to offer digital asset loans

Only offer such products following a review of the 3AC fiasco – such will highlight the importance of only issuing fully collateralised/over-collateralised loans + each loan comprises <10% of the loan book

Learn-To-Earn

Crypto teams pay Kraken to advertise/educate users. Once a user watches a video, they are paid out in that team’s native cryptocurrency. Coinbase already offers this.

Services/products related to managing DAO treasuries

As DAOs continue to mature, offering services such as OTC, governance voting, and treasuries could be interesting for Kraken. Over the long term, this could spin out or partner with exchanges looking to capture some private market investing capabilities ahead of new-age IPOs

Prime Brokerage Service

subscriptions, zero-fee trading, $$$ account protection, insurance against theft, automated tax services

NFTs and the tokenisation of everything

While more abstract, Kraken should position itself on tables where financial institutions and entertainment bodies are creating NFT standards for the tokenisation of products and services, both financial and otherwise. Should the technology come, Kraken should aim to have a seat on the table

7. Competition

Kraken’s main competitors are other CEXs such as Binance, Coinbase and FTX, and crypto wallets such as MetaMask.

Centralised exchanges

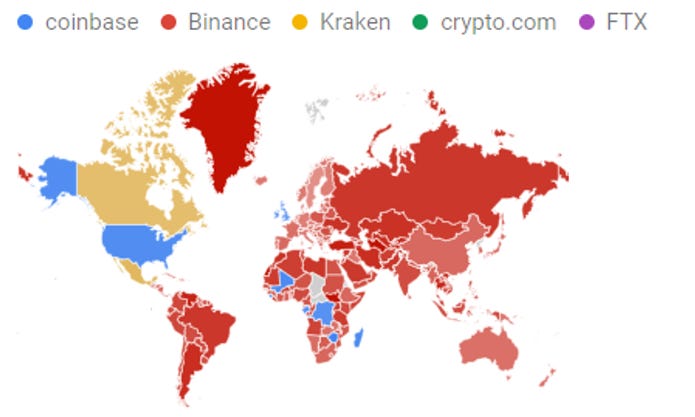

The variety of regulatory regimes and difficulty of cross-border transactions worldwide has resulted in a fragmented market of region-specific crypto exchanges – Coinbase (9m users) and Gemini (5m+ users) in the US, Kraken (5m users) in Europe, Bitso (5m users) and Mercado Bitcoin (3.8m users) in South America, YellowCard (1m+) in Africa, Huobi, Binance (c.29m users), OKEX (20m users) and Bitfinex in Asia, Rain (0.2m users) and Bitoasis (0.2m users) in the Middle East. Naturally, there is overlap.

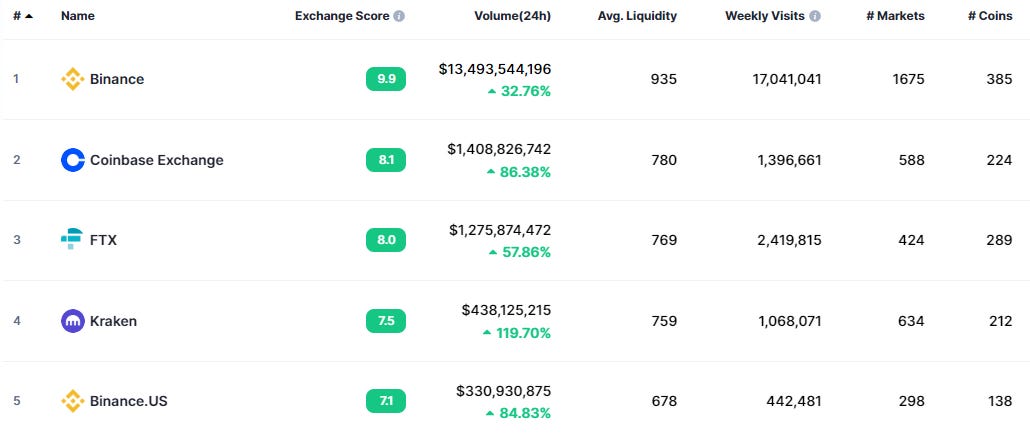

The above shows the cryptocurrency spot volume of a typical day. Binance is heads and shoulders above the rest with Coinbase being multiples more than Kraken despite having <10% of Binance’s volumes.

Relative to some other exchanges, Kraken has grown slowly. Binance and FTX were founded after Kraken and both are larger and growing faster. A reason for this could be the breadth of services and trading capabilities offered.

For instance, above is a screenshot of Binance’s app. Other platforms offer exotic instruments such as tokenized stocks, prediction markets and leveraged tokens. None of which Kraken offers. Similarly, while other players have aggressively invested in marketing, Kraken has avoided this.

Decentralised exchanges / Crypto Wallets

Armed with a crypto wallet, users can engage with decentralised exchanges (DEXs). These are self-executing smart contracts for trading. Coupling liquidity providers (users receive trading fees for this) and a token, the equation of x*y=k, allows for trading without an order book. Trading volume on decentralized exchanges (below) reached c.$1.5 trillion in 2022.

8. Valuation

We value Kraken at $2bn - $5bn. We have considered valuations to date for CEXs (both public and private) and used Coinbase valuation to drive this. Light review below. Our valuation is driven by precedent transactions and Coinbases’ share price evolution.

CEX Valuations

Crucially, these valuations occurred in 2021 and (practically speaking) will be materially marked down today. We estimate these are broadly down 40-60%. Bakkt is down 90%+ since IPO…

Unlike its competitors, Kraken has not recently raised meaningful capital. Its last funding was via a $13m raise via crowdfunding in 2019 at an alleged c.$4bn valuation. It is impressive that they are self-funding. Kraken’s earlier valuation rounds are unclear. Kraken has raised just c.$120 million in venture capital, significantly less than Coinbase ($547M) and FTX ($1.8bn).

Due to this, Kraken is likely underfunded and may not have significant capital reserves. Similarly, Kraken was rumoured to IPO at $10bn in early 2021. This was around when Coinbase had a market cap of $65bn. With Coinbase being down 75% since, Kraken would be valued at c.$2bn pari passu.

9. Conclusion

Kraken is an interesting company that has the raw ingredients to be a leader in the crypto space. However, this may require a pivot. As an exchange, Coinbase and Binance have significant advantages that seem insurmountable.

Any formal engagement would require information and data on the following topics:

Kraken’s user metrics and retention over time

What is the current cash runway for Kraken?

What percentage of total revenues is trading related?

What is the blended transaction fee % for users? How do fees differ for institutional investors?

What is Kraken’s current plan to reach profitability in the medium term?

Kraken reportedly wants to hire new staff while others are reducing their head count. What is the rationale for this and how do you consider the costs?

How does Kraken plan to increase mindshare in the crypto winter?

What is the product roadmap for the next 3 months, 12 months?

How much does Jesse own of Kraken? What is the current shareholder ownership register?

If you like my work, please reach out - @711_Joseph