The Bank of Apple

The Bank of Apple

Apple's 3rd Act | BNPL and saving products don't make sense....until they do....

Hi All,

Recently I’ve been fascinated by Apple's foray into financial services.

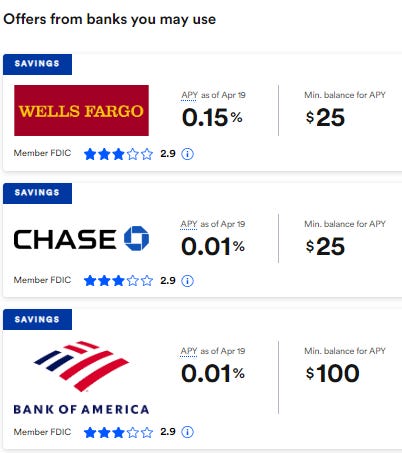

First, it was the announcement of their “Pay Later” feature. That was already interesting. It’s similar to BNPL but its ideology is very different (spoiler!). Now Apple is offering a savings account with 4.15% per cent APY via its “Wallet”. This compares to the average US savings account rate of 0.37%!

The question is….why?!! You’re already giving away almost all economics and the pay later feature is free for consumers to use.

While my curiosity may strike you as much ado about nothing, I’ve spent 20+ hours reading/researching and well….I think I’ve found the answers to Apple’s strategy. Thankfully, the level of nuance is extremely satisfying. Let’s dive in.

I explain the what, consider the why, and conclude with some predictions…

Not advice. Conversational starters only…

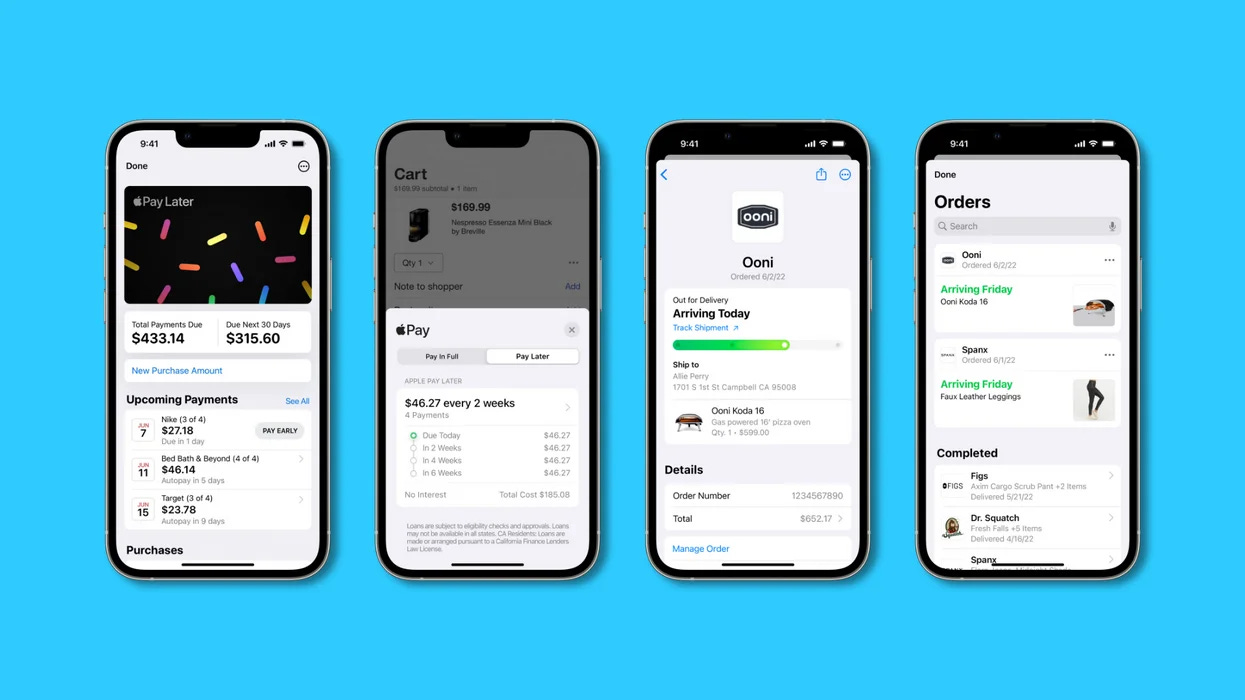

The What(let)?

Apple Pay Later

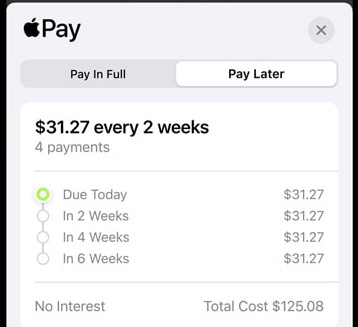

Apple recently launched their Pay Later feature (U.S. only). Here, users can split their purchases into four payments - one at the time of purchase and then one every 2 weeks - spread across 6 weeks. They change zero interest and have no fees.

A soft credit check is done during the application process to help ensure the user is in a good financial position before taking on the loan. Users can also apply for Apple Pay Later loans of $50 to $1,000.

Here, Apple owns the user interface, while the backend financials are powered by Goldman Sachs

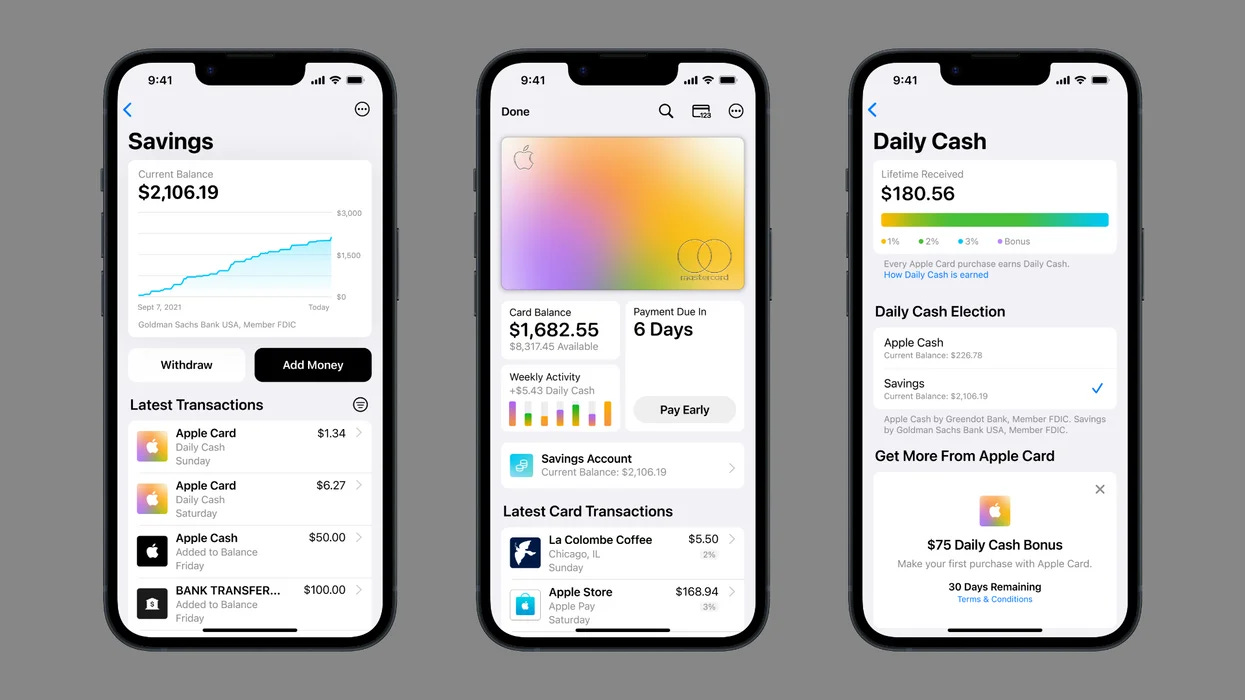

Apple Savings Product

Apple also offers high-yield savings account paying out 4.15% APY - 10x the national average. Goldman is again the technical issuer of the loans (official BIN sponsor) while Apple makes the loans directly to the user via is subsidiary.

iphone Distribution

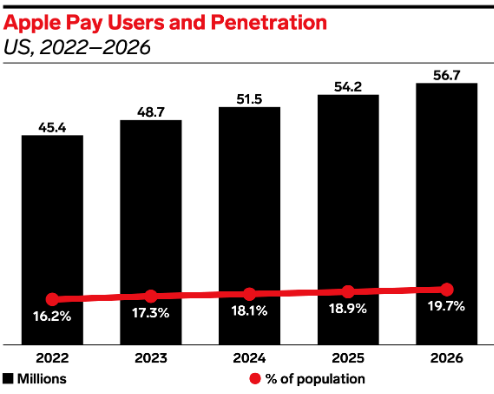

Research suggests that more than 1.2bn people have iPhones! In the US, 45.4m people use Apple Pay. That’s 16.2% of the population. I estimate that globally, 10% of 1bn+ iPhone users use Apple Pay - I am one of them. 100m+ willing customers is impressive.

The Why

Both halves of this section will set the scene for my predictions…

1. “But they’re making no Revenue?!”

That was my gut reaction.

Last year, Apple made almost $400bn revenues! With a gross profit of $170bn (Annual Report). Excluding all the hardware, services (Apple Care, cloud, digital content, payments etc.) make up $78bn in revenues! As you will see, Pay Later and Saving Accounts are a drop in the ocean relatively.

BNPL Revenue Opportunity - Pay Later Revenue Generation

BNPL companies make money by charging merchants 2-8% of the purchase amount. Sometimes they also charge interest to customers, a flat fee from merchants and late repayment fees (more ad-hoc).

JPM analysts forecast that the total US BNPL spend will reach $180bn by 2025. Presuming a 3% fee per transaction, the US BNPL market size is $5.4bn. Apple would need 18.5% market share to touch $1bn revenue. Not only is this unlikely (Klarna and co are fierce!) such revenues are a rounding error for Apple.

Interest Income Revenue Opportunity - Saving Account Revenue Generation

Banks make money by taking deposits and loaning them out. They pay customers an interest APY (let’s say 1%) on their deposits. Then charge loanees a higher interest rate (let’s say 3%). Their revenue is thus, 3% - 1% = 2%.

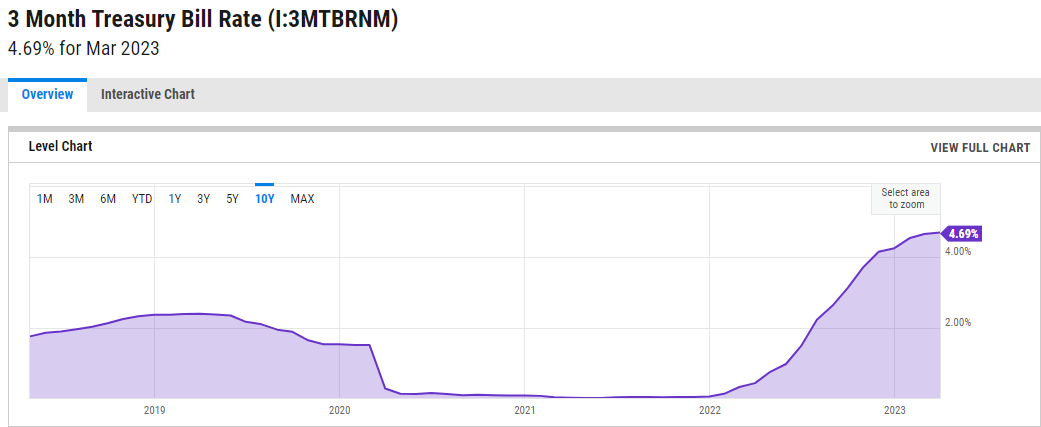

The banks can also invest deposits in certain assets (let’s not go into what they can/can’t invest in - google “CET1 Capital” if you’re interested, or dm me). They could invest in 3-month T-Bills from the government (IOUs to the US government).

Hence revenues are 4.69% - 1% = 3.69%.

As you can see, the name of the game is to give depositors as little as you can.

N.B.: Banks have to be very careful and selective with who they give loans. They could try to price their loan costs super high but only people with “risky” credit profiles would pay that much. As you go up the risk scale, the chance of blow-up increases. This is why you see neobanks be really careful and rarely give out loans. It’s an art!

While competitors pay depositors peanuts - as you can likely attest to, reader (!) - Apple is coming to disrupt the status quo with a massive 4.15% pai back to depositors.

This is an obvious mechanism to increase users while eating some % points. Apple does not charge for its loans. Our formula is now:

Interest Income from T-Bills - Interest Expense = Net Income = 4.69% - 4.15% = 0.54%

This is again a drop in the ocean for Apple. To make $1bn, Apple would need $185bn in deposits. This would place them as the 13th largest bank deposit taker in the US!

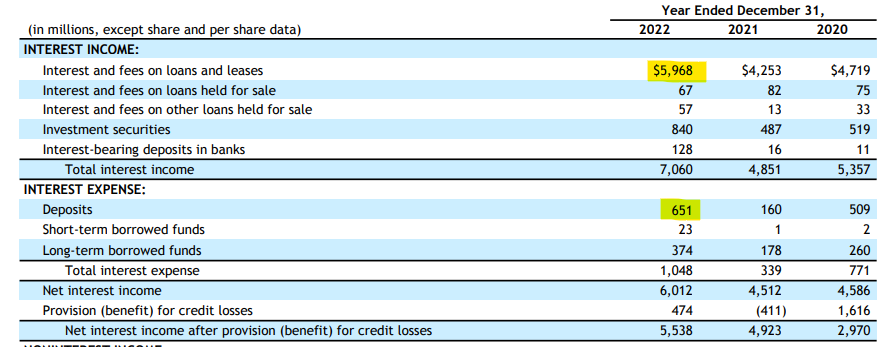

To drive the point home that Apple is being super disruptive, we can look at Citizen Bank. It had $181bn of deposits in 2022 …

….Yet pays $651m to depositors while it uses their $ to make $6bn! If they were paying all depositors 4.15% like Apple, they’d be paying out $7.5bn!!! Scenes.

Apple Pay Revenue Opportunity

For completeness, simply using Apple Pay also nets a fee for Apple. They take a 0.15% nominal cut from processing services to the issuer bank. Otherwise, it is free to use for consumers and merchants.

This is genius - Apple Pay massively reduces friction and guarantees a secure transaction. Naturallym it has drummed up lawsuits. But this is not why we are here so let’s move on.

As I’ve laboured above, Apple is obviously not looking at Pay Later or Saving Accounts as revenue generators.

Apple would need significant market share in a fierce BNPL space to make $1bn (unless the market grows significantly). This is unlikely in the short term

Apple pays out so much to depositors, it needs to be a top 15 deposits collector to make even $1bn

2. So what is Apple Trying to Do?

Apple’s approach is much more nuanced.

Payments is Apple’s 3rd Act

By now, Apple has conquered both software and hardware:

I don’t understand how anyone would choose an Andriod over an iPhone

I use my AirPods for over 25hrs each week

I love the Apple software/user interface (need I go on more about automatically pulling emailed “codes”)

In fact, Apple has already touched various industries - music, movies, fitness, and health

But now Apple is coming for our wallets…

BNPL is Out, Pay Later is In

Apple’s “BNPL play” is completely different to its “competitors”. BNPL and Pay Later are different animals.

While they have many similarities, BNPL players view consumers as their product. Their real target is merchants. You can see this as Klarna and Affirm pages/apps are basically a shopping discovery system. BNPL creates value for merchants.

Pay Later is focused on Apple’s users. They don’t care where you are, what you’re buying or even who you’re buying it from.

Instead, Apple’s playbook is…

Hook > Value add-ons > Grow Dependancy > Build distribution > Index Entire Economy level Profits

Use a hook product to capture and train users on their product. When you think of payments, you think of Apple Pay

Then you add value in easy/small ways. Apple did this using tickets, boarding passes and more. Below is my credit and debit cards, Arsenal membership and Tesco Club card. I love it when I have a boarding pass in there too as it makes travelling easy. Other examples are “get paid early” (Chime) or “real-time P2P payments” (CashApp).

Now add new features to grow the dependency. Pay Later increases the users’ reliance on Apple via utility while the saving product becomes a place where you park value that is important to you. I expect P2P payments and broader loans from Apple soon

At this point, you own the customer and then look to scale. With its monster distribution - again, 1.2bn people have iPhones. All about distribution and grow the % of iPhone users using Apple Pay.

Finally, you dictate terms and claw a fee for everything. Apple’s master plan is to fundamental index the whole economy. If transactions are happening, they want to take a cut. Finance is clearly the next big lock-in. Not even open banking would force them to share data with competitors

By stage 5, Apple has built a business that not only rivals Paypal ($83bn market cap), and Block ($38bn) but you even start to eat Visa’s ($481bn) and Mastercard’s ($358bn) dinner.

Suddenly, Apple has a new segment adding $100bn+ to their sum-of-the-parts valuations. Financial domination… Apple Style.

Predictions & Musings

To close, I’ll leave you with some predictions

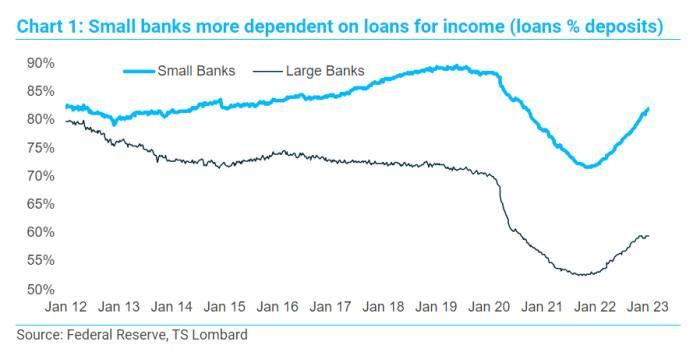

1. Apple will be a benefactor of the post SVB world & retail depositors’ flight to safety

After the collapse of Silicon Valley Bank, there was a massive rotation of deposits away from regional banks (and investment platforms like Charles Schwab) to the Big 4 banks. This is because there was is a belief that the US government would always bail them out.

JPMorgan Chase led the pack with $37bn in new deposits in the first quarter, bringing total deposits to $2.38tn! Meanwhile, Apple has a $50bn cash ($23.6bn cash and $45bn liquid securities) pile. $50bn!

It’s tough to know how many deposits other neobanks have but the biggest neobank, Revolut has a valuation of $33bn (£7.4bn deposits in 2021) while the US player Chime has a valuation of $25bn!

In other words, Apple will comfortably hoover up deposits as not only is it a brand that is well trusted/loved by many but they have the FUNDS to support themselves against a bank run.

Besides, as finance grows inside the behemoth of Apple, Apple Bank does not need to rely on NIM generation in the short term…unlike smaller regional banks (below)

2. Open Banking will unlock BNPL/Lending

I’m already quite bullish on open banking but concede that at current levels, its promise/monetisation has been disappointing. Still, I think that open banking is key to unlocking BNPL/consumer lending at scale.

For instance, you’re trying to buy a pair of $90 Nike Trainers. Rather than performing a soft or hard credit check (where the latter can impact your credit score!), open banking can be used. It would simply review users’ transaction history/current balances across their cards. Such can be used to generate a user’s profile and hence a educated decision on financing is made.

In fact, Apple’s acquisition of Credit Kudos for $150m (raised $5m in their 2020 series A) immediately provides this capability to Apple. In addition to data aggregation, it has specialist tools that harness users’ data to construct affordability and underwriting models. An obvious buy for Apple.

3. Apple is still in Kindergarten

Again, Apple Pay Later allows customers to split their payment into 4 equal payments over 6 weeks. This is much faster than its largest peers:

Klarna offers 3 monthly instalments or pay-in-30-days

Affirm offers 4 interest-free payments every 2 weeks or long-term monthly repayments

Afterpay offers 4 instalments over 6 weeks too but also offers long-term monthly repayments

This allows for a super quick credit cycle. Similarly, its loan offering of only $50 - $1,000 is tiny! Apple quickly gets payment data from its users and learns what good/bad customers look like. Much better than risking it all with a larger 1-year loan!

Similarly, as Apple Financing makes its own credit assessments and improves its credit engine, it could initially bundle and sell its credit facilities to larger institutions. This is a far cry from other players (Lendable in the UK) that only have the assessment engine!

With its high volume and a strong balance sheet, Apple’s credit and profiling algorithms will learn incredibly fast and can learn from its mistakes.

Conclusion:

Apple is going for their 3rd act. By giving away easy economics, it rapidly builds its data engine, trains users to use its platform and eventually will be able to tax the entire economy wherever payment transactions occur.

Thanks for reading, God bless.

Joseph - 21st April 2023