PayPal, Stablecoins and Finance 3.0

PayPal, Stablecoins and Finance 3.0

Let's find out just how *stable*...PayPal is! (I couldn't help it...)

Hi All,

As you’ve probably seen by now, PayPal has announced the launch of its stablecoin, PayPal USD ($PYUSD). It marks a significant step towards institutional adoption!

The coverage I've seen so far has been bland and superficial. It’s time to change that. Below are some of my thoughts. I'll start by discussing the high-level concepts (what and why) and then delve into the details by considering the first derivative impacts.

Let’s dive in.

My opinion only. Not the views of my employer. At best entertaining and at worst educational (hopefully!)

Background (feel free to skip)

Stablecoins are magical internet money digital tokens with a “value” of $1. You can think about them as an “IOU”. Its creator promises that on a certain blockchain, you have a digital token that is “good for” $1. You can redeem that $1 at theoretically any time.

There are 4 types of stablecoins; we will be focused on the first one (personally I would never hold any of the other types)

Fiat-Backed: Stablecoins backed by real-world currencies/treasuries in a 1:1 ratio

Commodity-Backed: Stablecoins that use commodities (physical assets i.e. gold) to provide their price stability

Crypto-Backed: Stablecoins that use one or more cryptocurrencies as collateral (i.e. a BTC reserve - see Terra)

Algorithmic : Stablecoins that use algorithms to control their supply and achieve marketplace stability (see Terra again)

While the value of the stablecoin de-pegging is a real concern, the stablecoin market has ballooned to $117bn (Defilama) and is forecast to hit $2.8 Trillion by 2028 (Bernstein Projects). So it’s no wonder PayPal got in on the action…

The What

PayPal, has launched its own stablecoin, PayPal USD ($PYUSD). Here’s the low down:

The stablecoin will be issued by Paxos Trust, a crypto infrastructure provider

As alluded to earlier, $PYUSD is fully backed by US dollar deposits and short-term Treasuries

$PYUSD users will be able to transfer funds across PayPal accounts and integrated wallets (think Venmo and merchants eventually)

$PYUSD will initially live on the Ethereum network allowing users to transact with the coin outside of the PayPal ecosystem

PayPal currently supports only Bitcoin, Bitcoin Cash, Ethereum, and Litecoin on its platform

Most importantly, the assets are Bankruptcy remote, meaning that customer assets are fully segregated (New York banking law) and if Paxos is ever insolvent, customer assets

willmay not be used to cover Paxos’ debts

From Sept-23 Paxos will publish a monthly Reserve Report for PayPal’s stablecoin. This outlines the composing of the USD reserves backing the token

The Why Now

In many ways, this is a no-brainer move from Paypal. As the first corporation to launch a stablecoin, PayPal has both the first mover advantage (land grab) but also an early bet into a financial product that - I think - has what it takes to change the fabric of society.

I think about the “Why” in 3 parts:

More Transactions Less Problems

Merchants Swear Fealty To PayPal

Net Income

Fundamentally, PayPal makes money via (i) helping consumers to transfer money (pay for products and services/P2P transfers etc.) and (ii) helping merchants with their digital checkouts. In FY22, it had 435m active accounts (transacting 51.4 times on average a year) across 22.3bn global transactions and $1.4 Trillion total payment volume. PayPal is a payments behemoth.

My thesis: The use of stablecoins will proliferate. Hence, by owning more of the infrastructure where money is transacted, PayPal indexes American/global financial transactions, capturing more of the pie. This means that they increase both their payment volume and the blended take fee; while crucially owning the underlying data by tracking the usage/wallet/profiles transacting using their token.

1. More Transactions Less Problems

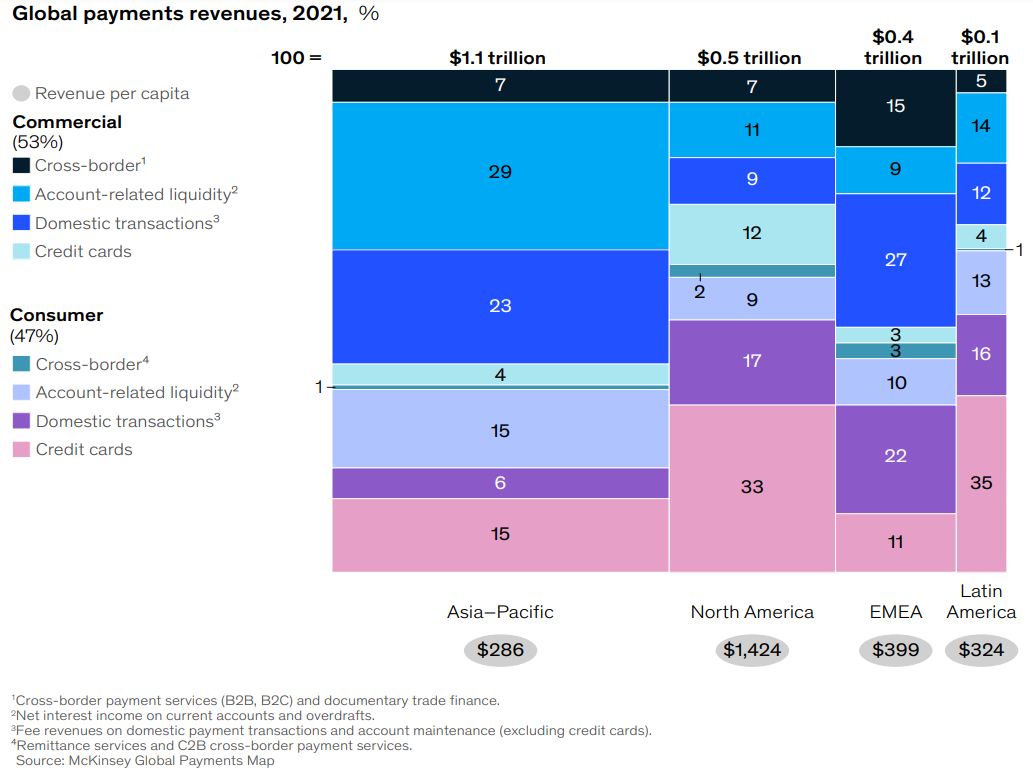

In FY22, PayPal made $25.2bn from transactions alone. This compares to Mckinsey & Co’s 2022 global transactions revenues of $2.3 Trillion; suggesting that PayPal has a market share of 1.1%. Still, there remains untapped opportunity with Mckinsey estimating that the global transactions reach $3.3 trillion by 2026! Capturing an extra 1% is meaningful for PayPal.

Bain & Co. also predicts that digital currencies have the potential to affect 5% to 10% —or more—of the global payments market by 2030. Hence, the digital currencies revenue opportunity is at least +$300bn

In the short term, if PayPal’s stablecoins can leverage existing payment infrastructure to accelerate time to market and maximize simplicity of on-boarding and usage, PayPal could be on to a winner here. After all, PayPal has a strong footprint across the world and more importantly has customer trust - its almost theirs to lose.

2. Merchants Swear Fidelity To PayPal

The introduction of stablecoins enables PayPal to empower its 35m merchants (of 435m active accounts). For instance:

Access to credit solutions: PayPal can visualize users’ transaction history of $PYUSD and form an educated view on credit offerings (BNPL or overdraft)

Fraud prevention/risk management solutions: PayPal and the authorities would readily use Etherscan/Chainalysis et al. to monitor fraud accounts. Requiring KYC for access to its stablecoins would also help this massively

Data analytics to attract customers and improve sales conversion: Similarly, being able to track users and thus help merchants to better target customers is a material benefit

3. If Coinbase Does Net Income Why Can’t PayPal

Finally, as Coinbase knows well from its tie up with Circle and USDC (see below), in the L12M to H1’23 results, 27% of Coinbases’ revenues came from its interest income profit split generated by the yield in the $$$ backing USDC.

To help us speculate, we can first assume that a stablecoin’s market cap equals the amount of $1 in the creator’s bank. Tether has $83.3bn, USDC has $25.8bn, Binance USD is $3.4bn.

In fact, to break into the top 5 and top 10 for fiat backed stablecoins, $PYUSD would need to issue $500m and $50m respectively. Not only does this show that Tether is by far the leader here, it gives a runway estimate of $5bn - $50bn for eventual PayPal $PYUSD deposit in the medium term. Assuming rates settle at 3%, that an extra $150m - $1.5bn in revenue just for building out more infrastructure functionality.

N.B.: For the vigilant, a question that you may ask is how does PayPal fund this? They have $10bn cash as of H1’23. Well, KYC verified users - an exchange, institutional investor, individual trader or business merchant - can deposits fiat currencies into PayPal, receiving $PYUSD in return.

To sense check, Tether’s recent attestation says that in Q2’23, its excess reserves (read as net interest income!) grew by $850m ($3.4bn run rate; on $83.3bn Tether tokens) suggesting a c.4.1% interest rate which sounds right. Hence out potential revenue upside for PayPal sounds about right.

Thanks to rising interest rates, $PYUSD has become a viable product for PayPal to pursue. At the size of PayPal, $PYUSD is effectively a CBDC but launched by big-tech rather than a Central Bank.

First Derivative Thoughts

So with the what and the why out of the way, we can think deeper on the impacts of PayPal releasing a stablecoin. Here, more than a few things come to mind:

PayPal and the graduation from “Checkout”

The proliferation of digital wallets as ID

The conundrum of settlement time

Dollarisation of EM economies & enabling financial inclusion

Data is King

+++

1. PayPal and the graduation from “Checkout”

PayPal’s bread and butter is its checkout experience for customers. While it does a good job, it is still far from its golden grail of users saying “PayPal It” vs “send it on PayPal”.

Though its network function via word of mouth + its online proliferation is strong, looking into the future, PayPal must (I say must as I think this deeply but honestly, just my personal opinion) go up the customer experience stack and live “lower” in the food chain.

For instance, below you can see the customer shopping experience.

By coming up through to the browsing and discovery level (as it has kind of started with Honey - *wink* *wink *nudge* *nudge*), PayPal would increases both its cut of fees and transaction volume, but also be data rich.

Stablecoins are a unique opportunity to do this due its natural requirement for a digital wallet to transact. Imagine this, each user has a self-named wallet (see Ethereum Names Sevice) that works like below.

A digital wallet that can transact with stablecoins and other currencies as necessary, but is also connected to the Driving License database, has NFTs that act as access keys to online services/products, single log in (eat your heart out Apple!).

To come back, PayPal can own this stack and track users using Stablecoins as the launch pad. Not to mention with the rise of embedded payments, consumers could effortlessly make micro-payments for media, services, or goods seamlessly across platforms.

And all of this is if PayPal wants to go at 1,000 mph. It could also start with a stablecoin only wallet where DLT and crypto addresses are hidden

2. The proliferation of digital wallets as ID

Similarly to the above, a single digital wallet that has been pre-approved (or without going into weeds, can use zero-knowledge-proofs) would help tremendously as KYC and identity versifiers could now exist on a blockchain. If I use “Simeon.eth”, you’re going to know it’s me. Paper-work and re-submitting be gone!

You’d never have to re-submit ID or permissions or fund documents or go through paperwork to access financial products offered by tech savvy institutions. Instead, the digital wallet can be check for credentials. Online social groups would BOOM but that’s for another post!

3. The conundrum of settlement time

One challenge with Ethereum or Bitcoin is that they’re not instant. If I wanted to buy an apple from a store, before the transaction settles on the blockchain, the value of the Apple could have moved materially. I argue that for stores, they don’t mind a c.10 min settlement as long as the value stays the same. Stablecoins are perfect for this.

While I hear you scream - “Joseph you can already do this with FIAT!” Sure. But I see a future where merchants vastly prefer digital wallets because:

More efficient/cheaper cross-boarder payments (rip cross-border payment companies charging crazy fees)

Faster international settlement

Better FX transparency

Working capital innovation of stream accounts receivable/payable rather than bullet payments

I could go on!

4. Dollarisation of EM economies & enabling financial inclusion

The amalgamation of the previous points and considerations for the volatility in currencies from emerging markets makes the point clear - USD is a safe currency of choice and a digital version created from a reputable company carries serious weight.

Today, anybody with a smartphone and internet access will be able to hold, send and spend fiat currency via stablecoins. Such is the product market fit here that Turkey, China and some African/Latin American countries have taken a hard line approach to crypto. In other words, widespread use of stablecoins as a savings account vs. local currencies would significantly hurt banks in the region.

5. Cash Data is King

Simply put, a $1 note is fungible. If you had a stack of 1,000 notes, it is not trivial to find the original. However with tokens and stablecoins, each token has an ID and can be tracked bouncing across wallets.

Stablecoins bring unique technology to the fore amidst a backdrop of often - technical term here - janky financial services infrastructure. Its a miracle that quadrillions of dollars successfully moves around the wand and works!

BUT. Financial contracts live in PDFs saved on desktops. Middle & back office cost in banks and tech firms runs into the billions! A lot of these things should be straight forward and automated. I.e. ‘who bought what when’ or ‘which payment belongs to which trade’ should be trivial.

While I was going to add some more “Second Derivative Thoughts”, I’ll do that in the next blog! Spoiler: Tokenisaion and Stablecoins as a platform.

So what Is Next

For PayPal, its been one of the worst-performing stocks in the NASDAQ - down 17% YTD despite wider up tick in the wider index and S&P driven by tech stocks. Still, I admire their bravery in tackling Stablecoins head on.

Though there are some teething issues such as users concerned about code that allows Paxos/PayPal to freeze or wipe an account (a common feature of other stablecoins - see Dune for USDC’s a banned wallets - but the future looks promising.

For me, 4 Questions remain:

How will issuers maintain stablecoin operations in a reduced interest rate environment?

What are the underlying risk of de-pegging if the collateral is poorly-managed or a USDC-Silicon Valley Bank style event happens?

Will PayPal keep deposit costs at zero or would they be tempted to offer users of $PYUSD some interest?

Also its not all glitz-and-glam, numerous countries are actively exploring CBDCs and these may compete with $PYUSD not to mention ongoing regulation updates.

In conclusion, PayPal has opted to be the first mover by introducing its own stablecoins. While its yet to be seen how successful it is - especially considering that Facebook Meta failed.

As usual, I’d love to discuss more and hear your thought. Message me on Twitter/X (@711_Joseph) and we can take it from there!

For now, thanks for reading and God Bless

Joseph - August 2023

Good summary Joseph! I appreciate your time getting this together.