How to buy a Distressed US Bank

How to buy a Distressed US Bank

J.P. Morgan made HOW MUCH over a weekend?!!

Hi All,

Recently I’ve been engrossed by Warren Buffet’s shareholders’ letters. One of the most popular phrases has become an idiom in its own right:

Every investor goes through a Warren B phase. For me, reading the above from the 1986 letter (link) was somewhat perfect timing. It explains what happened to Silicon Valley Bank & First Republic Bank.

(I explained what happened to SVB in >1,000 words here)

NOT ADVICE. ONLY MY OPINION.

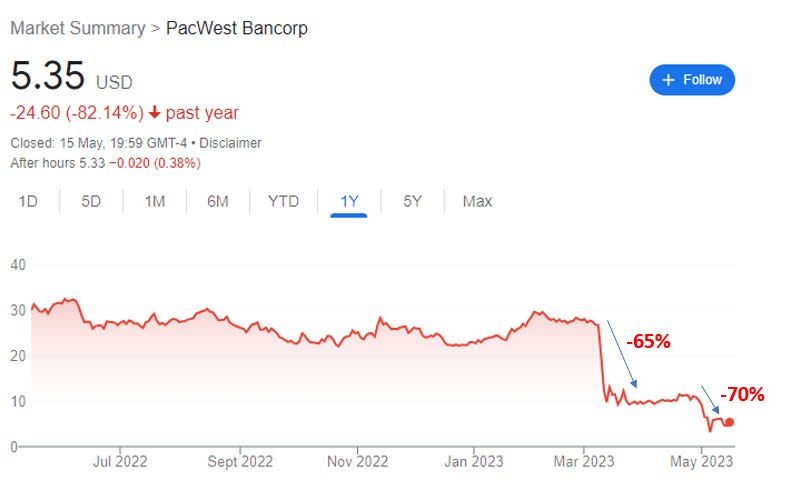

As you’ve undoubtedly seen the world is ending massive banks are failing. From Signature Bank to Silicon Valley Bank, First Republic Bank and even the precarious position of PacWest Bancorp.

In fact, I thought it was only crypto where you can see your position lose -60% twice! Ouch indeed.

Following many years of MAX GREED, the toxic concoction of (i) the end of the low-interest rate era, (ii) oversized investing in long-term fixed-income securities, (iii) frictionless deposit flows, (iv) increasing inflation, and (v) increasing costs, have REKT banks.

Yet. While many banks are now in MAX FEAR mode, some savvy banks are collecting face-melting returns.

J.P. Morgan Makes $8bn!

7th May-23, JPM announced its acquisition of most of First Republic Bank’s (FRB) assets. This came after a week of panic and significant deposit outflows at the bank. Gone are the days of people lining up outside a bank to withdraw their hard-earned money. Today, this happens at the speed of light (or at least your internet connection).

Once rumours of default begin to spread, withdraws began at an astonishing rate, as indeed FRB discovered.

By the end of Dec-22, FRB had $176.4bn of deposits…

… As of the Friday before it collapsed, FRB had only $92.6bn deposits, a c.50% decrease!

In fact, excluding the $30bn in deposit donated from a group of third-party banks as a last-minute lifeline, FRB would have only $62.6bn deposits, a remarkable c.60% decrease.

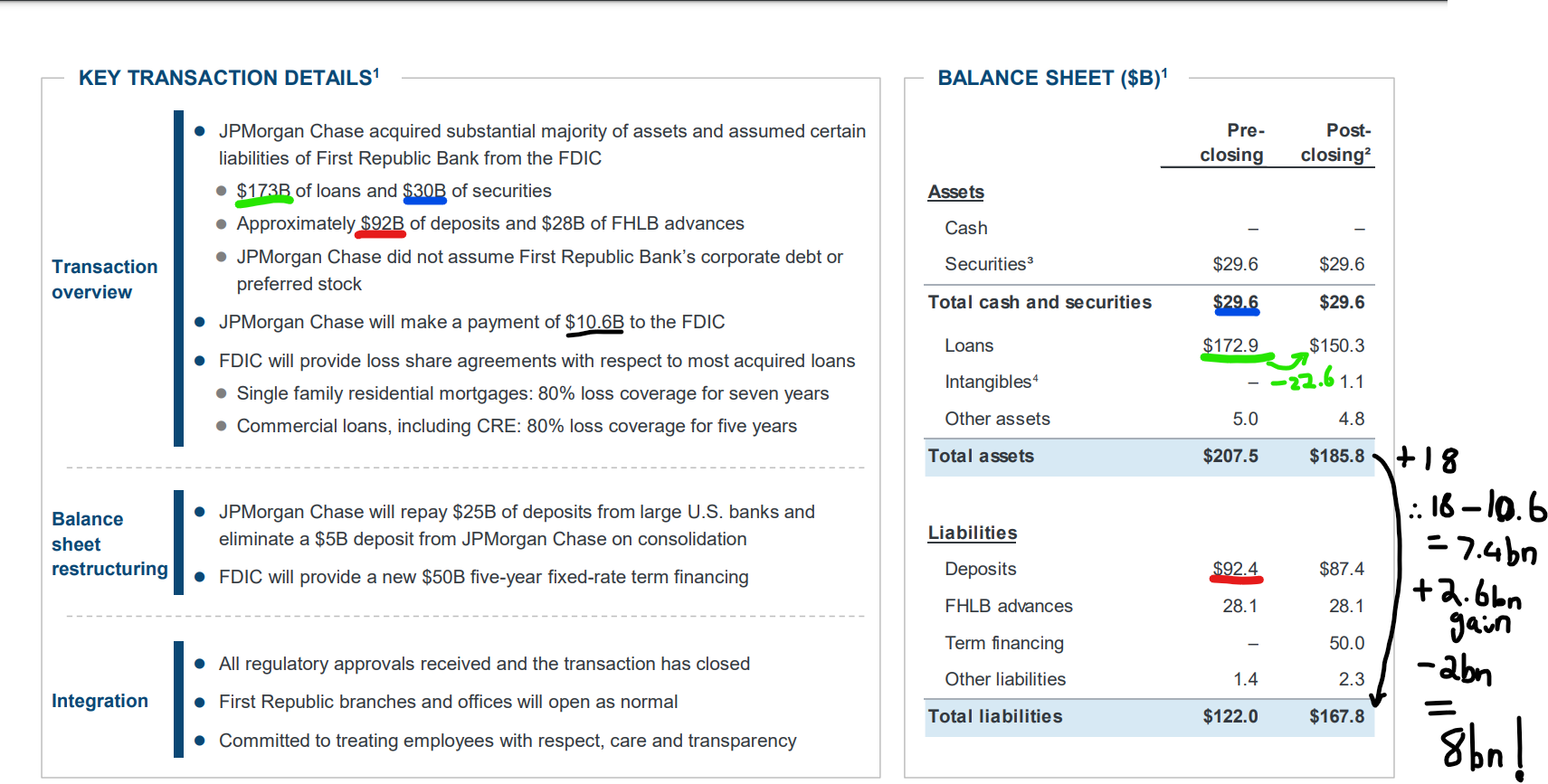

So what were JPM’s acquisition terms?

Terms

JPM acquired the “substantial majority” of FRB’s assets.

This included including c.$173bn of loans and c.$30bn in securities

It also acquired c.$92bn in deposits. This included the aforementioned $30bn of large bank deposits (repaid post transaction close)

JPM established a loss share agreement with the FDIC. This protected JPM from any losses associated to FRB’s single-family residential mortgage loans + commercial loans and the FDIC provided $50bn of fixed-rate term financing for the next 5 years

JPM leaves First Republic’s corporate debt and preferred stock behind, marking these to zero.

As a result of this transaction, JPM expects to pick up $2.6bn post-tax at closing (excludes the $2.0bn restructuring costs (FY23-FY24).

It also picked up FRB’s branches and offices. JPM also keeps the staff that it didn’t sadly fire. FRB’s wealth management platform will become part of J.P. Morgan Advisors

What a steal! Basically, they pick up $8bn worth of value (maths below), almost $100bn in deposits (excluding people leaving FRB to swap deposits to JPM directly!) and build their wealth platform massively. ALL OVER ONE WEEKEND.

Ladies and gents, this is a masterstroke from Jamie.

Other Points:

To achieve this feat, shareholders are of course wiped out. As were corporate debt or preference shares holders.

The FDIC pays a pound of flesh and has marked a $13bn loss. This is charged to the Deposit Insurance Fund.

The FDIC would agree that it is s a reasonable price to pay for saving the bank’s depositors. Following the transaction, FRB customers could use J.P. Morgan’s Chase Bank network and it was rapidly biz as usual.

To J.P. Morgan’s credit, it did band together the initial $30bn to try and save FRB

It is surprising that the likes of Goldman didn’t bid for the loans. Having interned in their sales & trading division, I am loosely certain that they have more than what it takes to buy them at a nice discount and then hold and opportunistically sell down the book

Other Bank Heists

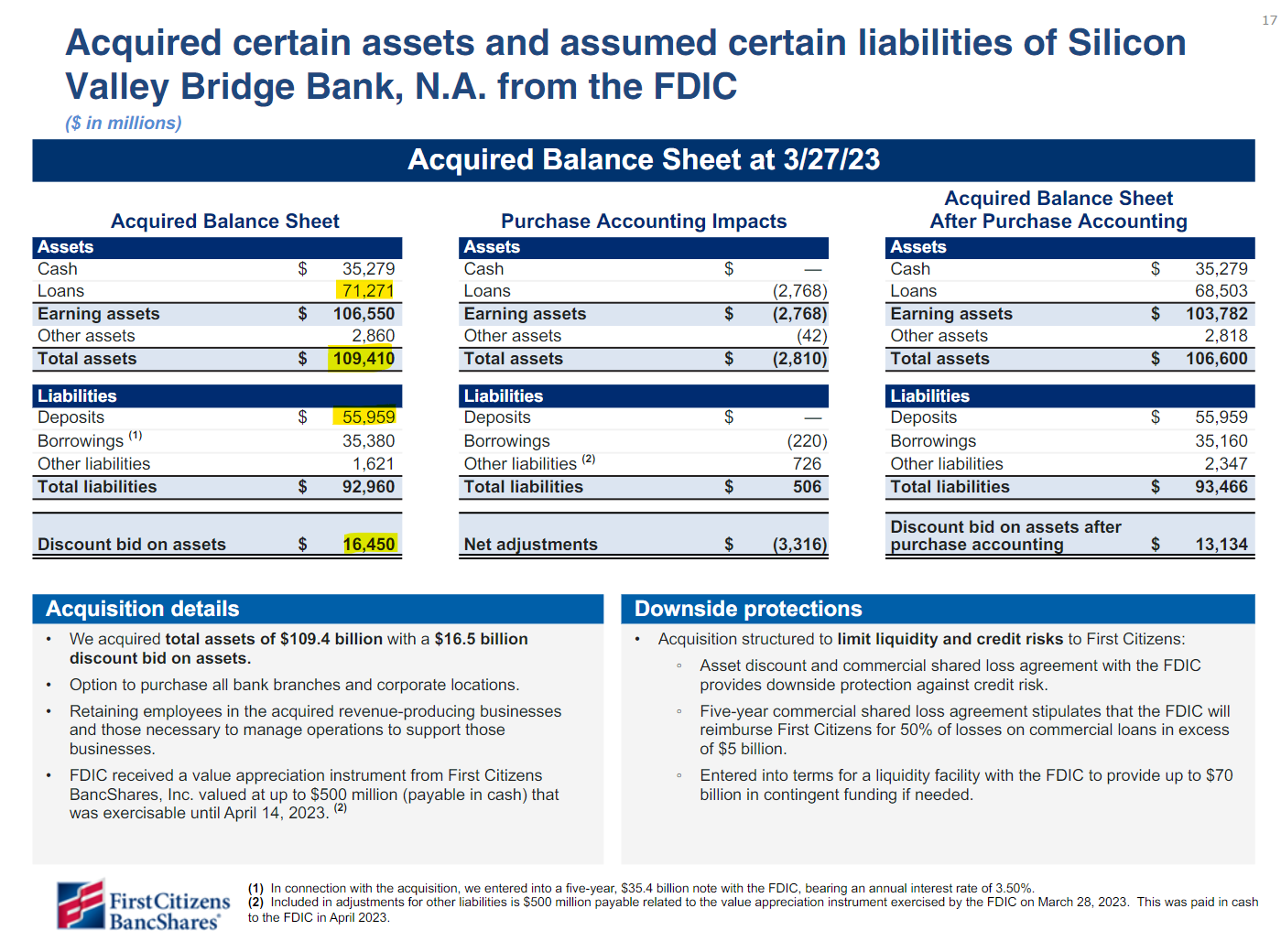

SVB was bought by First Citizens Bank.

Acquired c.$110bn assets, c.$71bn loans, and $56bn deposits. It also agreed on a loss share agreement with the FDIC. They pocketed $16.5bn (discount to assets) and $9.8bn in income from this transaction in just Q1’23. Eye-watering!!!!

“Thanks for playing!” I can faintly hear them scream to shareholders. All-time highs…

+++

Interestingly, the FDIC publishes the other SVB bids here. There were 4 realistic bids (taking the whole loan book and deposits) yet two of them didn’t even have a loss share agreement in their offer! Duh! I won’t go into detail but from the list of offers, you can really tell that First Citizens are very savvy.

What’s more, other bidders included private equity (Apollo, Blackstone and Sixth Street) as well as startups like Brex Inc.!

In other heist news, PacWest Bancorp recently sold $2.6bn in fixed-income securities for a c.$200m discount!

From all of this, Warren is right. Have a fortress balance sheet and be greedy when others are fearful!

Further reading:

Signature Bank Post Mortem | https://www.fdic.gov/news/press-releases/2023/pr23033a.pdf

In summary, ^ these failures were caused by a combination of:

(i) Poor risk management. i.e. SVB regularly broke its own internal limits and then fiddled with them to make them look better

(ii) Concentrated deposit bases - 60 clients represented 40% of Signature’s total deposits. 4 depositors represented 14% of total assets!

(iii) Long-dated fixed-income instruments locking in a death spiral amidst the rapid speed of depositors’ flows

Conclusion

It PAYS to be patient. For now, I’ll ignore the perils of being a CEO of a publicly listed company with a “black swan war chest” - activist investors will oust you and demand dividends! - but clearly, it PAYS to be the right bank, at the right time.

Thanks for reading.

Joseph - 2nd June 2023

I'm always open to exploring these topics and others in more depth. If you'd like to continue the conversation, feel free to reach out to me on Twitter (@711_Joseph)