Chewing a Gorillas | The 10 Minute Battle For Stomach Share

Chewing a Gorillas | The 10 Minute Battle For Stomach Share

Musings about food delivery, Getir's acquisition of Gorillas and predictions for the sector...

Hi All,

Ever since the meteoric rise of Ocado & Uber Eats, I’ve been fascinated by last-mile grocery delivery. In short, it’s a problem that has left start-up carcasses in its wake and billions of VC $$$ burnt.

However, the industry cannibalization continues! Getir has acquired its grocery app rival Gorillas in a $1.2bn deal. I love a good consolidation play.

This blog thinks about last-mile “instant” grocery delivery, the transaction and my predictions for the sector.

Enjoy!

+++

These are my views only and do not reflect my employers’. Entertaining at best and hopefully at least a conversation starter!

+++

Problem

While incumbents such as the Tesco and Ocado of the world offer (i) ‘click & collect’, (ii) same day/next day grocery delivery or (iii) delivery within time slots at pre-planned times, these are slow.

Cash-rich, time-poor consumers want “instant” groceries without leaving their homes!

With residential areas sitting closer to shopping areas, and European culture being one of many weekly shops during the week vs a weekly “big shop”, it is little wonder that stars began to align for the birth EU based unicorns.

Solution

Quick delivery, “Q-commerce”, is a class of startups that soared during the pandemic. They offer close to instant delivery of general groceries. Its instant gratification-commerce pitch is simple:

Via a network of strategically located mini-warehouses or ‘dark stores’, q-commerce companies deliver groceries in >15 minutes.

After going mainstream in the lockdowns of 2020/2021 and being won over by its convenience, for many, this new style of shopping out of necessity has become a habit - I am one of the users! In the last year, I’ve used Gorillas c.10 times and Deliveroo 150+.

It’s a model that combines an app, a network of mini-warehouses, pickers & packers, a fleet of drivers and software. Idealistically, these start-ups save costs with bespoke real estate in tier-2 locations.

The first derivative outcome that you’d expect is increased efficiency with better unit economics than traditional supermarkets… as we will find out, it’s harder than it sounds!

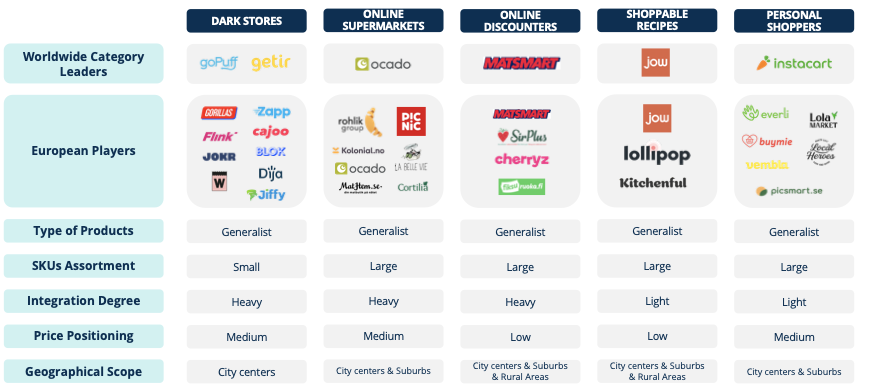

Below, we will focus on Q-commerce companies with dark stores. A helpful separation as there are many types of food delivery companies (i.e. online supermarkets/discounters, meal kit providers or ethnic food offerings)

I will exclude regional players like Rohlik group (Czech Republic, Hungary, Austria, Germany, Romania, Italy and Spain), MatHem (Sweden) and Oda (prev. Kolonial - Norway).

It’s not all rainbows…

Similarly to the global backdrop, Q-commerce companies have felt the pain. Buyk, Fridge No More and Zero Grocery have closed down, Jiffy and Vembla have pivoted away from delivery and lay-offs are commonplace.

Gorillas let go of 300 employees and plan to exit Italy, Spain, Denmark and Belgium. UK, Germany, France and the Netherlands remain

Getir announced a 14% cut to staff but did not reduce its footprint. It operates in UK, Germany, France, Italy, Spain, Netherlands, Portugal and the US

Zapp is set to cut headcount by 10% - estimated to be 200-300 employees

GoPuff reportedly laid off 2,500 people earlier this year (3% in March and a further 10% in July and 250 customer service staff in October), and has closed 75+ warehouses in the US

Ouch!

Acquisitions Central

When costs are simply too much, consolidation is the classic play. In Q-commerce consolidation is not new. In recent memory, there have been several acquisitions though these had an expansionary rationale.

Getir Acquisitions:

Blok | Expansion into Spain and Italy (Jul-21)

Weezy | UK expansion plans (Nov-21)

GoPuff Acquisitions:

Fancy | UK expansion plans (May-21)

Dija | Competition take out (UK) and expansion into France and Spain (Nov-21)

Congrats to these founders for exiting after just 8 months!

Other:

Cajoo acquired by Flink | Expansion into France and partnership + investment with retailer Carrefour (May-22)

Frichti acquired by Gorillas | Increase coverage in France and operational know-how (Jan-22)

Flink raised a $750 million Series B (not a typo!) at a $2.1bn valuation. Led by Doordash (Dec-21)

My instinct is that all of these M&A transactions were completed at valuations <$150m.

The remaining players in Europe are GoPuff, Getir, Zapp, and Flink. Including their acquired entities, they have raised >$5b to date!

Transaction Rationale | Getir & Gorillas

Getir has acquired Gorillas, valuing the combined group at $10bn. Admittedly, I had thought Gorillas and Fink would merge.

The deal values Gorillas at $1.2bn, down from its $3bn valuation in Sep-21. But Getir also has taken a valuation bath. Despite hitting an $11.8bn valuation when it raised c.$800mn in March, Getir is now valued at c.$8.8bn (88% of WholeCo).

On the face of it, this deal makes a lot of sense…

Cost Synergies

These synergies are crucial as Gorillas was rumoured to have spent €1.50 for every €1!

Anecdotally, you could game them by filling a fake basket (not completing the order) and get rewarded with ‘one-off’ discounts the next day.

Significant overlap in services across Europe means:

The network of city-based dark stores is rationalised, resulting in fewer locations and more efficient processes

Job and real estate cuts as fewer delivery drivers and head-office staff are needed

The companies have offices in cities including London, Paris, Amsterdam and Berlin

Lower marketing costs, reducing the customer acquisition costs

Benefits of scale with an improved negotiation point with suppliers

Reduced costs of technology. While there will be integration costs, merging talent and tech should reduce long-term R&D spending

Revenue Synergies

Revenues synergies would only stem from an improved operational playbook. In other words, city scaling know-how would improve. They’d also be able to strengthen coverage of cities and increase market share.

Investor Returns

While this mostly stock acquisition will be disappointing for Gorillas’ investors - Delivery Hero, Coatue Management, Tencent and DST - it comes with a $40m-$100m cash sweetener.

Looking to the Future | New Partnerships & Improved Business Models

It’s a tough time for Q-Commerce but there could be a happy ending (financial sustainability and scale).

To move to profitability, Q-commerce players will need to extend their proposition beyond the core of urgent/distressed buys.

Partnerships

Supermarkets

Armed with logistics and data, Q-Commerce players are purpose-built to compete on the new retail battlefields. But the longer-term data expertise of incumbents could be invaluable. The likes of Tesco could also help with (i) warehousing know-how, (ii) usage of part of their current real estate for warehousing and deliveries and (iii) improving negotiations with suppliers. A good example of this is Flink’s relationship with Carrefour and Rewe (Germany).

For supermarkets, this could be an opportunity to get their own-brand products into dark stores and leverage the opportunity for exclusive product launches/testing. They could also sell their less popular brands or bundle offers thereby reducing discounting.

Food-Delivery

Traditional food delivery players will naturally try to eat a piece of the pie. For instance, Deliveroo has launched Hop, a grocery delivery service, in partnership with supermarkets Morrisons and Waitrose.

This has already begun to playout:

Just Eat Takeaway.com (JET) and Getir announced a pan-European partnership announced last month (Nov-22). Getir’s app will be embedded into JET’s

GoPuff and Uber agreed to expand their US partnership to London

Doordash is a key investor in Flink

Predictions | Business Model Shift

I have several predictions for potential improvements in the Q-commerce business model…

A significant shift from “Instant” to “Ultra Fast” (longer waiting times)

Introduction of ‘Micro-stores’ for office-based employees

Increase of own-brand and brand spin-off offerings

Subscription services

Virtual Concierge

Raising even more $$$

Continued Consolidation?

Let’s dive in…

Migration from “Instant” to “Ultra Fast”

The 10-15 min grocery delivery is rarely relevant.

Simply put, the cost of delivery is unlikely to decline substantially. The economics of last-mile delivery is extremely challenging across sectors. This is made even worse by setting expectations for speed. Customers value predictable commerce over fast commerce. Indeed, 10 minutes is great but I would happily receive my grocery in 40 minutes!

Q-commerce players can encourage users to “go-green” or offer faster deliveries at a premium. As long as these deliveries stick to the time indicated it is an acceptable practice.

One approach may be to start offering more delivery options – hourly slots, same day, next day – and introduce a charging model with it.

Micro-stores

Via partnerships with real estate developers and employers Q-commerce players can launch bespoke micro-stores. For instance, within my employer’s intranet, I would be able to do my shopping (lunch or groceries) and order it for delivery in the building. This saves significant time and taps into impulsive orders. I already collect my evening deliveroo in the loading bay…

This also enables bulk orders across the office (increased efficiencies) and saves customers’ time.

Own-brand / Brand-spinoff

In addition to adding “Tesco’s Finest” and “Waitrose Essentials,” I predict Q-commerce alternatives to become commonplace. Similarly, the potential to leverage brand equity via restaurants’ own-brand ingredients may be lucrative. Consumers look to valued brands regardless of meal occasion.

Subscription

A subscription fee that offers free delivery on all orders and generates points on orders above a predefined level. This increases frequency and basket size. Points may give coupons etc. This makes discounting more manageable while improving economics for the cohorts.

Virtual Concierge

Drivers may be used more efficiently via partnerships with private healthcare and laundry services. A world where my medicine, dry cleaning, groceries and dinner are all delivered to me doesn’t need too much imagination.

Hungry for Capital?

Getir will undoubtedly come to raise money again. While its investors - Mubadala, Sequoia Capital and Tiger Global - have deep pockets, they’re going to have a tough time even at a $10bn valuation. And that’s IF Getir can improve profitability and generate money.

Considering Deliveroo’s and Just Eat Takeaway.com’s treatment in the sleepy London Stock Exchange, I predict any IPO would should be in the US.

Continued Consolidation?

On a Whole.Co take-out level, I think this is unlikely. The remaining players are simply too big. Consolidation is still possible however via Q-commerce companies exiting counties.

Strategic acquirers - food delivery companies - are the only alternative exits other than IPO. Though Just Eat Takeaway’s acquisition of Grubhub is a cautionary tale.

Publicly traded food delivery companies have all seen their share prices fall 50%+ in the past 12 months. However, interestingly, they have A LOT OF MONEY.

Uber - $4.9bn in unrestricted cash with a further $4.4bn in equity stakes

Doordash - $3.8bn in cash, cash equivalents and short-term marketable securities

DeliveryHero- €2.9bn in cash

Grab - $5.0 bn in net cash (cash, cash equivalents, time deposits and cash investments)

There is a history of country-only exits - Takeaway.com’s acquisition of DeliveryHero’s German operation (brands Lieferando, Pizza.de and Foodora) for €930m. They now have a 100% market share as Deliveroo and Uber exited the market. Marketing decreased in the periods immediately after too.

It is certainly a painful period for Q-commerce. I believe that these companies have a right to exist + opportunity remains should these businesses become profitable.

Till then, while the bright sparks of 2021 have dimmed, the industry will remain red hot. Not one for VC but maybe… just maybe… ambitious management teams can make it a success.

That’s all folks! Thanks for going on this journey with me! Let me know what you think below or @711_Joseph.

I’ll reward myself with a Nandos on Deliveroo… washed down with my San Pellegrino from my last Gorillas order!

Joseph - December 17th 2022